主にツイッターを舞台にしたサマーズとクルーグマンのインフレを巡る暗闘をこれまで何度か取り上げてきたが(ここ、ここ、ここ、ここ、ここ、ここ、ここ、ここ)、直近のツイートでサマーズがクルーグマンのツイートを正面から取り上げた。

I am glad to see @paulkrugman join the view that the American economy is overheated at present and in need of restraint. If overheating risks had been recognized more promptly, we would be in a less severe predicament today.

Yesterday I wrote about how a recession is possible but not inevitable, and that policy could err in either direction 1/ https://nytimes.com/2022/04/22/opinion/inflation-recession-federal-reserve.html

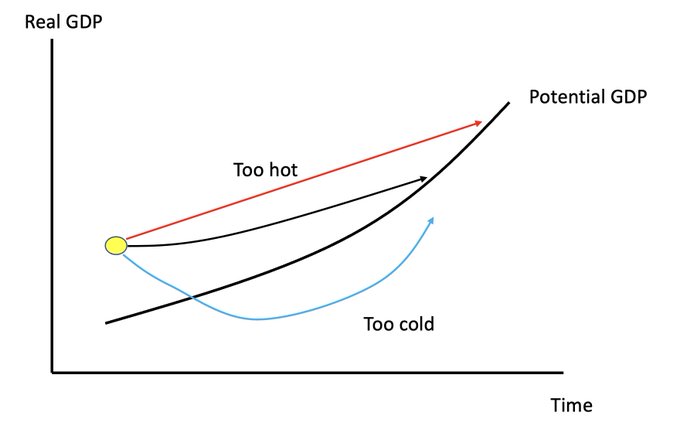

@paulkrugman is right to point out that as many of us have stressed there are 2 risks w an overheated economy. @federalreserve might tap the brakes too softly and allow inflation expectations to be entrenched or it might hit the brakes too hard & send the economy into recession

Krugman professes optimism about a soft landing. I’m not sure why. There are no examples of soft landings with inflation above 4 and unemployment below 4. We are well into this territory and have the additional challenges of the Ukraine war and supply shocks.

I judge the soft landing prospect in range of one third.

Note that contrary to @federalreserve forecast, @paulkrugman recognizes that inflation restraint, even in the Goldilocks scenario, requires increasing unemployment. As progressive @Claudia_Sahm has asserted, whenever unemployment goes up a little, it has always gone up a lot.

@paulkrugman seems to think @federalreserve is at risk of overdoing restraint. Possible. But it bears emphasis that even as forward interest rates over two years have soared, medium term expected inflation has risen.

I would be surprised if zero real rates, which is more than what is in prospect, are enough to reduce inflation.

(拙訳)

米国経済は現在過熱しており抑制が必要、という見解にクルーグマンが加わったのを見て嬉しく思う。もし過熱リスクがもっと早く認識されていたら、今日これほど深刻な状況に陥っていなかっただろう。Yesterday I wrote about how a recession is possible but not inevitable, and that policy could err in either direction 1/ https://t.co/fVLc5Swa8q

— Paul Krugman (@paulkrugman) 2022年4月23日

我々の多くが強調したように、過熱経済には2つのリスクがある、ということを指摘した点でクルーグマンは正しい。FRBがブレーキをソフトに踏み過ぎてインフレ期待が定着するのを許してしまうか、ブレーキを強く踏み過ぎて経済を不況に陥れてしまうか、だ。

クルーグマンはソフトランディングについて楽観論を述べている。私にはその理由が良く分からない。インフレが4%以上で失業率が4%以下の時に軟着陸した例はない*1。我々はその領域にかなり入り込んでおり、しかもウクライナ戦争と供給ショックという難題も加わっている。

ソフトランディングの可能性は1/3程度だと思う。

FRB予測とは逆に、ゴルディロックス・シナリオでもインフレ抑制のために失業率上昇が必要となる、とクルーグマンが認識していることに注意されたい。進歩派のクラウディア・サーム*2が述べたように、失業率が少し上がった時には結局は大きく上がるのが常である。

クルーグマンはFRBが引き締めをやり過ぎるリスクがあると考えているようである。その可能性はある。しかし2年以上のフォワード金利が大きく上がっているにもかかわらず中期のインフレ期待が上昇したことには留意すべきである。

実質金利ゼロは見通しよりも高めであるが、それでインフレを抑制するのに十分だとしたら驚かざるを得ない。

上記でサマーズがリンクしたクルーグマンのスレッドは以下の通り。

Yesterday I wrote about how a recession is possible but not inevitable, and that policy could err in either direction 1/

I argued that because inflation isn't yet entrenched, there is a "Goldilocks path" for policy, but staying on it will be tricky 2/

As it happens, Goldman Sachs just came out with a note (no link) making just about the same point. Key paragraph 3/

We don't want to underestimate how tricky this is. But while facile doomsaying may feel emotionally satisfying to the I-told-you-so crowd, it's not helpful. And we need to understand that there's a real risk of overreacting to inflation 4/

(拙訳)

昨日私は、不況の可能性はあるがそれは不可避ではなく、政策はどちらの方向にも間違い得る、という点について論説を書いた。

インフレはまだ定着していないため、政策の「ゴルディロックス経路」が存在するが、その経路を維持するのは難しい、と私は論じた。

たまたまゴールドマンサックスもまったく同じことを指摘したメモを先ほど出した(リンク無し)。主要部分。

それがどんなに難しいかは過小評価すべきではない。しかし、お手軽な破滅の予言は、言わんこっちゃないと言いたがる人々を感情的に満足させるかもしれないが、有益ではない。それと、インフレに過剰反応してしまうリスクが実際に存在することを我々は理解しておく必要がある。