CPIに住宅サービスが与える影響のラグの問題については、クルーグマンが頻りに強調し*1、「論敵」のサマーズもいち早く指摘してきた(かつ、クルーグマンはむしろ遅かったと揶揄してきた)ところであるが*2、マンキューも4/11付けの表題のブログエントリ(原題は「It's all about shelter」)で取り上げた。

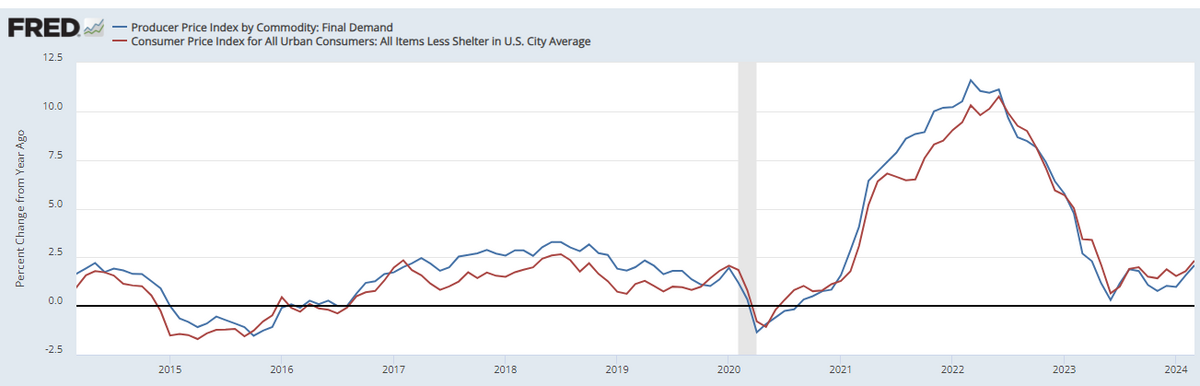

This figure shows that the PPI for final demand tracks the CPI less shelter very closely. By both measures, inflation is now very much under control. The problem is that the CPI for shelter is up 5.6 percent, so the overall CPI looks quite hot.

Some would argue that leaving out shelter is misleading because shelter is such a large fraction of the typical household budget. On the other hand, the CPI for shelter is well known to be a lagging indicator of rents by virtue of how it is constructed, and other more current series show no recent inflation in rents. This latter argument puts me in the optimistic camp on inflation.

By the way, I recently made a bet with my friend Larry Ball that the overall CPI from February 2024 to February 2025 will rise by less than 2.5 percent. I am writing the bet here as a sort of contract. We will check back next year.

The bet is for $5. That is in nominal terms. So, in real terms, I get more if I win than Larry gets if he wins.

(拙訳)

この図は、最終需要のPPIが、住宅サービス除くCPIを非常に良く追っていることを示している。両指標においてインフレは今や極めて良く制御されている。問題は住宅サービスのCPIが5.6%上昇していることで、そのためCPI全体がかなり過熱しているように見える。

平均的な家計の予算において住宅サービスは相当に大きな割合を占めているため、それを除外することは誤りだ、と論じる人もいる。一方、住宅サービスのCPIは、作成方法のために家賃の遅行指標となっていることが良く知られており、より一致性の高い他の系列は、直近における家賃のインフレを示してはいない。後者の議論により私は、インフレについて楽観派の陣営に参加する。

ちなみに最近私は、友人のラリー・ボールと、2024年2月から2025年2月までの総合CPIが2.5%以下に留まる、という賭けをした*3。ここにその賭けについて書くのは、一種の契約書としてである。我々は来年結果を確認する。

賭け金は5ドルである。これは名目値においてである。従って実質値では、私が勝った場合の獲得金額は、ラリーが勝った場合の獲得金額より多い。

今更感も強いが、CPI論争についてはマンキューが暗にサマーズではなくクルーグマン側に付いた格好である。

*1:cf. 瞬間インフレ率 - himaginary’s diary、クルーグマンのインフレあれこれ2 - himaginary’s diary。

*2:cf. 来たるべき住宅インフレ上昇 - himaginary’s diary、過去と現在のインフレの比較 - himaginary’s diary、コント:ポール君とラリー君――賃料と賃金をどうみるかの巻 - himaginary’s diary、コント:ポール君とラリー君――過去と現在の区別に気を付けようの巻 - himaginary’s diary。

*3:cf. コント:ポール君とラリー君――ボールらの論文をどうみるかの巻 - himaginary’s diaryで紹介したように、ボールらが2022年の論文で中央値インフレに重きを置いたことについて、中央値は住宅サービスを見ているに過ぎないのではないか、とクルーグマンが批判した。