というNBER論文が上がっている(ungated版へのリンクがある著者の一人のページ)。原題は「The Geography of Capital Allocation in the Euro Area」で、著者はRoland Beck(ECB)、Antonio Coppola(スタンフォード大)、Angus J. Lewis(同)、Matteo Maggiori(同)、Martin Schmitz(ECB)、Jesse Schreger(コロンビア大)。

以下はその要旨。

We assess the pattern of Euro Area financial integration adjusting for the role of “onshore offshore financial centers” (OOFCs) within the Euro Area. The OOFCs of Luxembourg, Ireland, and the Netherlands serve dual roles as both hubs of investment fund intermediation and centers of securities issuance by foreign firms. We provide new estimates of Euro Area countries' bilateral portfolio investments which look through both roles, attributing the wealth held via investment funds to the underlying holders and linking securities issuance to the ultimate parent firms. Our new estimates show that the Euro Area is less financially integrated than it appears, both within the currency union and vis-a-vis the rest of the world. While official data suggests a sharp decline in portfolio home bias for Euro Area countries relative to other developed economies following the introduction of the euro, we demonstrate that this pattern only remains true for bond portfolios, while it is artificially generated by OOFC activities for equity portfolios. Further, using new administrative evidence on the identity of non-Euro Area investors in OOFC funds, we document that the bulk of the positions constituting missing wealth in international financial accounts are now accounted for by United Kingdom counterparts.

(拙訳)

我々は、ユーロ圏内の「オンショアとオフショアの金融センター」(OOFCs)の役割を調整した、ユーロ圏の金融統合のパターンを評価した*1。ルクセンブルク、アイルランド、およびオランダのOOFCsは、投資ファンドの仲介のハブ、および、海外企業の証券発行センターという二重の役割を果たしている。我々は、2つの役割を通して見た、ユーロ圏諸国の二国間ポートフォリオ投資の新たな推計を提示する。その際、投資ファンドを通じて所有されている資産は本来の所有主に帰属させ、証券発行は最終的な親会社に関連付けた。我々の新たな推計が示すところによれば、通貨同盟内、および、ユーロ圏外との関係の両方において、ユーロ圏は見掛けほど金融統合が進んでいない。公的データは、ユーロ導入後にユーロ圏諸国のポートフォリオのホームバイアスが他の先進国に比べて急速に低下したことを示しているが、そのパターンは債券ポートフォリオにのみ当てはまり、株式ポートフォリオではOOFCsの活動によって人為的に生成されていることを我々は示した。また、OOFCsファンドの非ユーロ圏投資家の正体に関する新たな行政的証拠*2を用いて我々は、国際金融勘定において行方不明となっている資産を構成するポジションの多くは、今や英国のカウンターパートにおいて計上されていることを明らかにした。

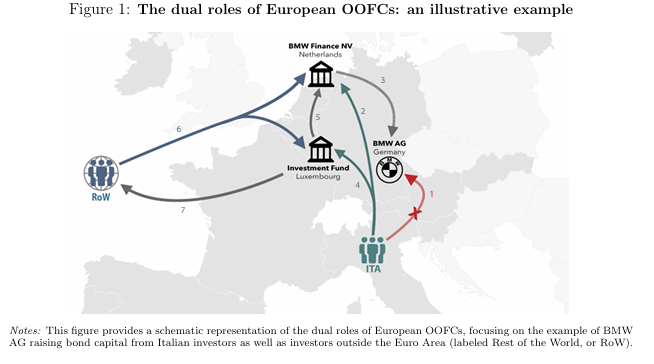

OOFCsが話をややこしくしている例として、論文では以下の図解を示している。

この例ではBMWが債券を発行してイタリアの投資家に販売しているが、通常想定されるような、ドイツで起債した債券をイタリアの投資家が買う、という経路(経路1)は取られない。実際には、オランダに籍を置くBMWファイナンスNVが起債し、それを海外投資家が購入する(経路2)。それによって調達された資金がドイツの親会社に貸し出される(経路3)。これはOOFCsが証券発行の場として機能する例である。

また、イタリアの投資家は債券を直接保有せずに、ルクセンブルクかアイルランドに籍を置く投資ファンドを仲介してポジションを持つ、という形にするかもしれない(経路4、5)。これはOOFCsが資金仲介のハブとして機能する例である。

ルクセンブルクやアイルランドはユーロ圏の投資家のみならず、ユーロ圏外の投資家によっても使われる。彼らはBMWファイナンスが発行した債券を直接買うかもしれないし、ルクセンブルクかアイルランドの投資ファンドを通じて買うかもしれない(経路6)。

さらに、ユーロ圏外の企業や政府がルクセンブルクやアイルランドで発行した証券をユーロ圏外の投資家が買うこともある(経路7)。これは「round-tripping」の一種で、海外からの投資は疑似的なものとなる。

そのほかの経路も国境を越えているので、ユーロ圏の統計上は国際投資となり、単純に集計すると二重計上となる。今回の研究ではそうした資金の動きを統合し、例えば経路2から5までの動きを単一のイタリアからのポートフォリオの債券投資とした、との由。

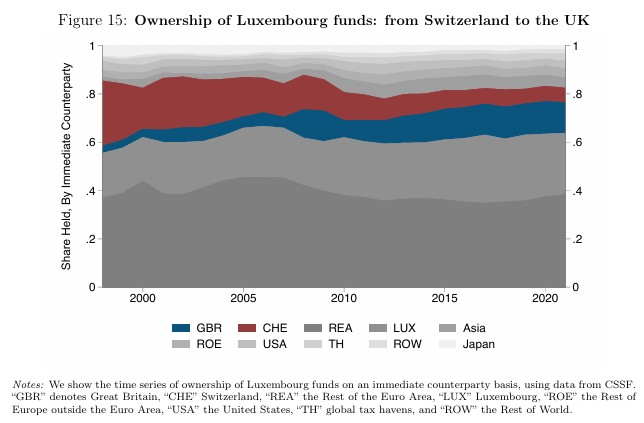

また、OOFCsファンドの非ユーロ圏投資家がここ20年でスイスから英国に置き換わってきたことを示す図として、論文では以下を示している。

このうちどれだけが英国居住者の投資で、どれだけが非居住者の投資かを厳密には分離できないが、居住者の投資もそれなりにあるだろうと論文では分析している。

*1:導入部ではOOFCsという用語について「...policymakers and researchers have long lamented that assessing European financial integration has proved difficult because of heavily concentrated financial intermediation activities carried out in Ireland, Luxembourg, and the Netherlands, whose scale has grown enormously over time... We refer to these three countries as “onshore offshore financial centers” (OOFCs), since they are onshore markets within the Euro Area, while at the same time their functioning parallels that of offshore financial centers. 」と説明している。

*2:アイルランド中銀とルクセンブルク金融監督委員会(CSSF)のデータを用いたとの由。CSSFについてはCommission de Surveillance du Secteur Financier - Wikipediaのほか監査監督上の協力に関するルクセンブルク金融監督委員会(CSSF)との書簡交換について:金融庁も参照。