というNBER論文が上がっている。原題は「Deposit Insurance, Uninsured Depositors, and Liquidity Risk During Panics」で、著者はMatthew S. Jaremski(ユタ州立大)、Steven Sprick Schuster(ミドルテネシー州立大)。

以下はその要旨。

The lack of universal deposit insurance coverage can create liquidity risk during financial crises. This aspect of deposit insurance is hard to test in modern data because of the broad coverage of most systems. We, therefore, study the role that the U.S. Postal Savings System played in commercial bank closures during the Great Depression. The system offered households a federally insured deposit account at post offices throughout the nation, and its structure provides a near-ideal environment to identify this competitive liquidity risk during a crisis. We find that banks that operated nearby a post office that accepted deposits were more likely to close between 1929 and 1935. We further make use of a structural change in the availability of postal depositories in the early 1910 to estimate an IV regression that confirms the results. In either model, the effect is strongest for those banks with low reserves, suggesting that the mechanism was through depositor withdrawals rather than other factors.

(拙訳)

全般的に預金をカバーする預金保険が無いことは、金融危機の際に流動性リスクを生み出し得る。今や大抵の金融システムでは預金を広くカバーしているため、預金保険のこうした側面を現代のデータで検証することは難しい。そのため我々は、大恐慌の商業銀行閉鎖時に米郵便貯金制度*1が果たした役割を調べた。同制度では、連邦政府による保険付きの預金口座を全国の郵便局で提供していて、その構造は、危機におけるそうした競争的な流動性リスクを識別するのにほぼ理想的な環境を提供していた。預金を受け入れていた郵便局の近くで営業していた銀行は、1929年から1935年の間に閉鎖する可能性が高かったことを我々は見い出した。我々はまた、1910年初めに生じた郵便貯金の利用可能性の構造的変化を利用し、この結果を確認する操作変数法による回帰を推計した。いずれのモデルにおいても、準備預金が低水準な銀行でその効果は最大となっており、同メカニズムが他の要因ではなく預金者の引き出しによって起きていたことを示している。

金融危機の不可思議な持続性 - himaginary’s diaryで紹介したJaremskiの論文と同様にエドワード・コナードがこの論文を取り上げている。

Jaremski and Schuster document that before the establishment of the FDIC, deposits fled to the safety of local insured postal banks, illustrating that lack of universal deposit coverage amplifies run risk. @ssprickschuster

Before the Federal Deposit Insurance Corporation (FDIC) became active in 1934, the only federally insured deposit accounts available to American households were through the U.S. Postal Savings System. To examine the role that postal savings played on bank closure, we collect the balance sheets of over 16,000 commercial banks just before the start of the Great Depression and match them with information on which post offices accepted deposits. We find banks that operated nearby a post office that accepted deposits were more likely to close between 1929 and 1935. The effect of postal savings is severely weakened after deposit insurance was installed across commercial banks in 1934. This lends evidence to the theory that we are capturing a competitive liquidity effect due to the lack of universal coverage.

(拙訳)

ジャレムスキとシュスターは、FDICが設立される前には、預金保険のある地元の郵貯銀行に預金が安全への逃避を行ったことを明らかにし、保険が預金を全般的にカバーしていないと取り付けリスクが増幅することを示した。連邦預金保険公社(FDIC)が1934年に活動を開始する前には、米国の家計が利用可能な、連邦による保険が提供されていた預金口座は、米郵便貯金制度によるものだけだった。郵便貯金が銀行閉鎖に果たした役割を調べるため我々は、大恐慌発生直前の16,000以上の商業銀行のバランスシートを収集し、預金を受け入れた郵便局の情報と突合した。預金を受け入れていた郵便局の近くで営業していた銀行は、1929年から1935年の間に閉鎖する可能性が高かったことを我々は見い出した。郵便貯金の効果は、1934年に商業銀行で預金保険が導入されると大きく低下した。このことは、我々が、預金保険の全般的なカバーの欠如による競争的な流動性効果を捕捉していたという理論の証拠となっている。

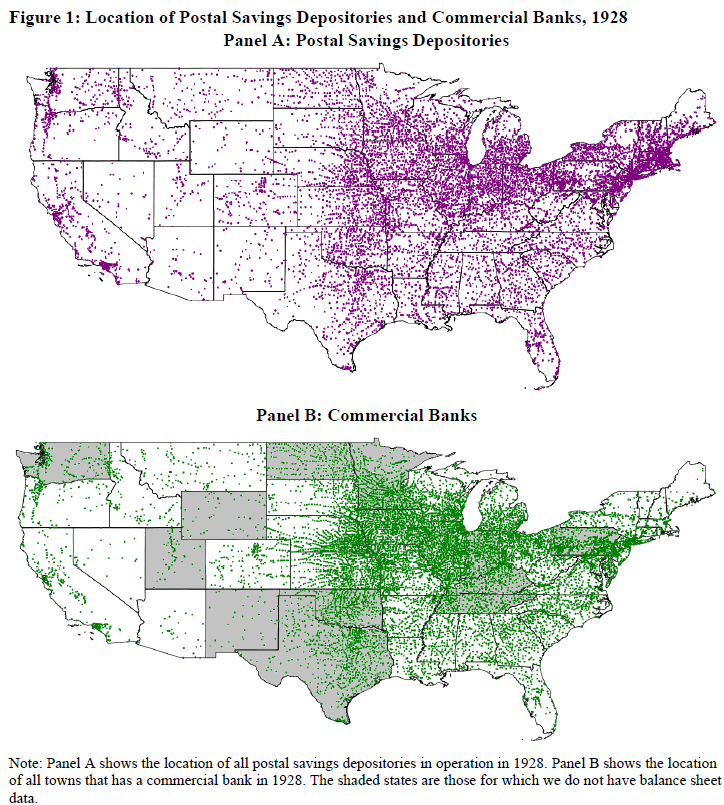

以下はコナードのサイトからの図の孫引き。