というエントリをサイモン・レンールイスが書いている(原題は「Could austerity’s impact be persistent」)。

If I could carry just one message into mediamacro to bring it more into line with macro theory, it is that nominal interest at their lower bound represent a policy failure. Unconventional monetary policy is a very unreliable substitute for interest rate changes and fiscal policy as a way of controlling the economy, and a temporary fiscal stimulus can reliably get interest rates off their lower bound. This was the big mistake that most advanced countries made in 2010, and painfully slow recoveries were the result. The UK is currently making the same mistake, which is why the macroeconomic impact of the Labour and LibDem programmes is so much better than the Conservatives’ continuing austerity.

In the textbook macroeconomic models, this policy mistake can have a large but temporary cost in terms of lost output and lower living standards. This is because in these basic models a short term lack of demand does not have an impact on supply. Output in the longer run is determined by the number of those wanting to work, the capital stock and technology, all three of which are assumed to be independent of short term demand shortages. However it looks increasingly like these textbook models can be wrong.

In a new study (pdf), Gustav Horn and colleagues at the IMK institute in Germany looked at how persistent the impact of negative fiscal shocks (higher taxes or lower spending) had been on output. Their analysis is a refinement of earlier studies by of Blanchard and Leigh, and more recently Fatas and Summers. They find that the impact of recent fiscal shocks have been persistent rather than temporary, at least so far.

Although this persistent impact is not part of textbook models, economists have explored effects of this kind (the collective name for which is ‘hysteresis’). There are many theories about why it could happen, such as theories of endogenous growth.

(拙訳)

メディアで流通しているマクロ経済学を本来のマクロ経済理論に近付けるために一つだけメッセージを送ることが許されるならば、下限にある名目金利は政策の失敗を表している、と言いたい。非伝統的な金融政策は、金利変更や財政政策に代わる経済調整手法としては、極めて信頼感に欠ける。一方、一時的な財政刺激策は確実に金利を下限から離陸させることができる。これは先進国の大半が2010年に犯した大きな過ちであり、結果として遅々とした回復に苦しんだ。英国は今また同じ過ちを繰り返そうとしており、それが保守党が継続する緊縮策よりも、労働党や自由民主党の政策の方が、マクロ経済に遙かに好ましい影響をもたらす理由となっている。

教科書のマクロ経済モデルでは、こうした政策の誤りは、失われる生産とより低い生活水準という形で、大きくはあるものの一時的なコストをもたらすであろう、とされている。というのは、それらの基本モデルでは、短期的な需要不足は供給に影響を与えないからである。長期的な生産は、働きたい人の数と資本ストックと技術で決まり、この3つの要因はいずれも短期的な需要不足とは独立であると仮定されている。だが、こうした教科書モデルが間違っている可能性が高まっているように思われる。

新しい研究(pdf)で、ドイツのIMK研究所のグスタフ・ホルンとその同僚は、マイナスの財政ショック(税の増加もしくは支出の低下)の生産への影響がどれだけ恒久的だったかを調べた。彼らの分析はブランシャール=リー、およびそれよりも最近のファタス=サマーズ*1というこれまでの研究を改善したものである。彼らは、少なくとも現時点では、近年の財政ショックの影響が一時的ではなく恒久的であったことを発見した。

こうした恒久的な影響は教科書モデルには導入されていないが、経済学者はこの手の効果を研究してきた(これらの効果の総称は「履歴」である)。内生的成長論など、そうした効果が生じる理由を説明する理論は数多ある。

この後レンールイスは、景気循環調整後の財政赤字をGDP比で1%削減するとGDPが恒久的に0.7%低下する、という仮定の下で*2、2010年以降の緊縮策により英国の2016/17年のGDPは本来よりも4%近く低くなった、という見積もりを示している。細かい内訳の数字や計算過程は示されていないが、断片的に示されている数字*3を総合すると、概ね以下のような計算をしているものと思われる。

| 各年マイナス幅(%) | GDP縮小幅(%) (←の累計) |

累積コスト(%) (←の累計) |

家計所得換算(ポンド) | ||

|---|---|---|---|---|---|

| 2011 | -1 | -1 | -1 | 760 | |

| 2012 | -1 | -2 | -3 | 2,280 | |

| 2013 | 0 | -2 | -5 | 3,800 | |

| 2014 | -0.43 | -2.43 | -7.43 | 5,647 | |

| 2015 | -0.43 | -2.86 | -10.29 | 7,820 | |

| 2016 | -0.43 | -3.29 | -13.58 | 10,321 | |

| 2017 | -0.43 | -3.72 | -17.3 | 13,148 | |

| 2018 | -0.35 | -4.07 | -21.37 | 16,241 | |

| 2019 | -0.3 | -4.37 | -25.74 | 19,562 | |

| 2020 | -0.3 | -4.67 | -30.41 | 23,112 |

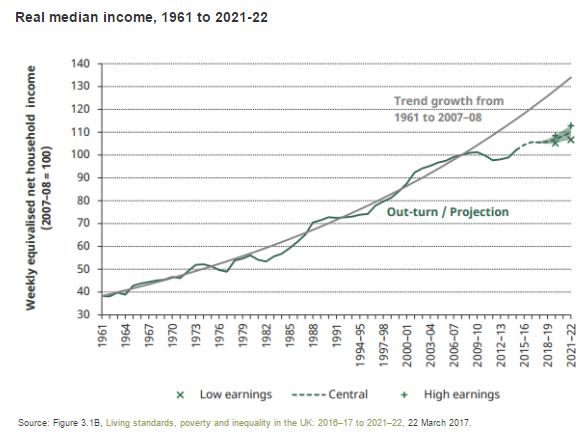

その上で、下図を用いて、現在の所得の中央値がトレンドよりも15%低くなっていることを指摘し、4%というのは決して大きな数字ではない、と述べている*4。

レンールイスはエントリを以下のように結んでいる。

I do not have to argue that such permanent effects are certain to have occurred. The numbers are so large that all I need is to attach a non-negligible probability to this possibility. Once you do that it means we should avoid austerity at all costs. In 2010 austerity was justified by imagined bond market panics, but no one is suggesting that today. The only way to describe current Conservative policy is pre-Keynesian nonsense, and incredibly harmful nonsense at that. That was why I signed the letter.

(拙訳)

私は、そうした恒久的な効果が確実に発生した、と論ずる必要はない。数字が非常に大きいので、この発生可能性について無視できない確率を与えさえすればよい。それができれば、緊縮策は何としても避けるべき、ということになる。2010年に緊縮策は、債券市場パニックという想定によって正当化されたが、今日ではそれを言う者はいない。今の保守党の政策を描写する唯一の方法は、ケインズ主義以前のナンセンスであってその点で信じられないほどの害がある、ということだけである。それが私が公開書簡*5に署名した理由だ。

*2:この0.7という数字は以前の推計と整合的になるように決めたとの由。小生はかつてこの数字を0.07と推計したことがあるが、そのちょうど10倍ということになる。ちなみに小生がこの0.07という数字をベースに行ったシミュレーションでは、消費税率の15%引き上げで各年のGDPが約1%低下するという結果になった。レンールイスはもっと小規模な緊縮策で同様のマイナス幅を導出しているものと思われる。

*3:具体的には次の通り:2013年で緊縮策の累積コストはGDPの5%(1+2+2)になり、家計当たりでは4,000ポンドになる。2016/17年のGDPは4%近く低くなり、2019/2020年までに予定されている追加的な緊縮策でさらに1%低くなる。家計の累積損失は2016/17年時点で13,000ポンドで、3年後には23,000ポンドになる。

*4:ただしこれについてコメント欄では、トレンドの取り方が恣意的ではないか、という指摘がなされている。