というNBER論文が上がっている(3月時点のWP)。原題は「What Drives Booms and Busts in Value?」で、著者はJohn Y. Campbell(ハーバード大)、Stefano Giglio(イェール大)、Christopher Polk(LSE)。

以下はその要旨。

Value investing delivers volatile returns, with large drawdowns during both market booms and busts. This paper interprets these returns through an intertemporal CAPM, which predicts that aggregate cash flow, discount rate, and volatility news all move value returns. We document that indeed these shocks explain a large fraction of quarterly value returns over the last 60 years. We also distinguish between the intra-industry and inter-industry components of value, showing that the ICAPM explains the former better. Finally, we develop a novel methodology to perform this decomposition at the daily frequency, using it to interpret value returns during the Covid-19 pandemic.

(拙訳)

バリュー投資は変動の大きいリターンをもたらし、市況が良い時も悪い時も大きな損失*1を招く。本稿はこうしたリターンを異時点間CAPMを通じて解釈する。その解釈によれば、総キャッシュフロー、割引率、およびボラティリティのニュースのいずれもがバリューのリターンを動かすと予測される。それらのショックが実際に過去60年の四半期のバリューリターンの大きな割合を説明することを我々は明らかにする。我々はまた、バリューの業種内および業種間の要素を区別し、ICAPMが前者をより上手く説明することを示す。また我々は、この分解を日次の頻度で行う新たな方法を開発し、それをコロナ禍期間中のバリューリターンを解釈するのに用いた。

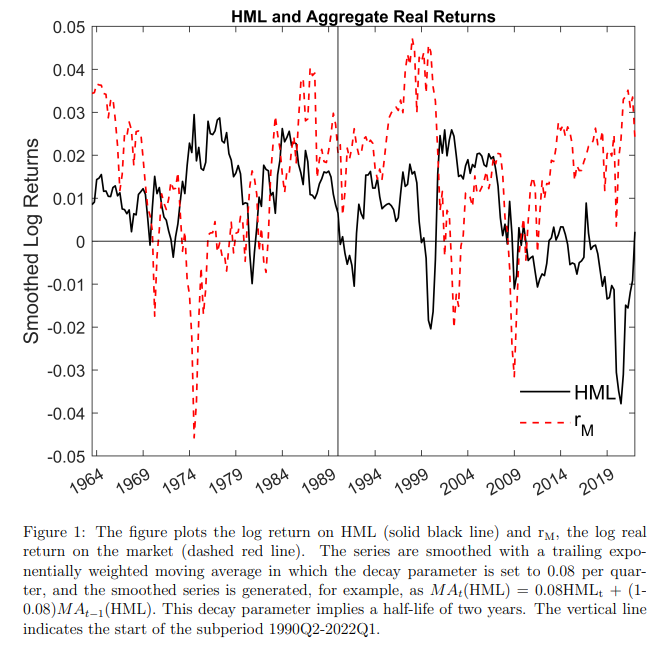

市況が良い時にバリュー株が損失をもたらした例としてWPでは、90年代末のITブームの時を挙げている(下図参照)。

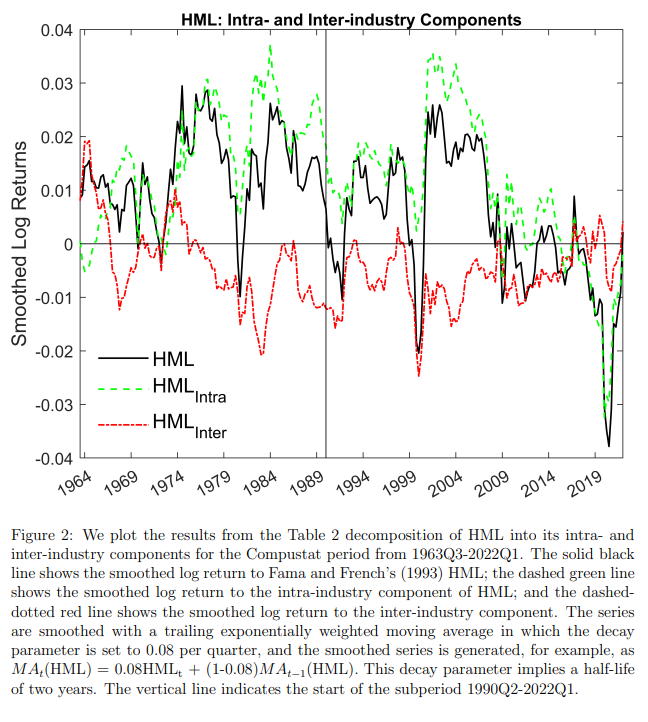

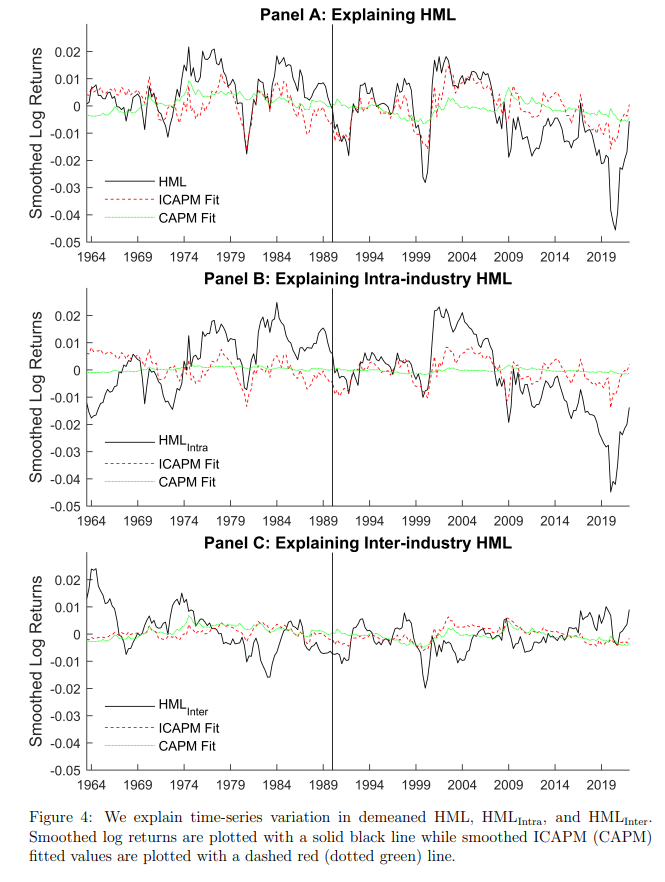

以下はバリュー投資のリターンを業種内と業種間に分解した図。

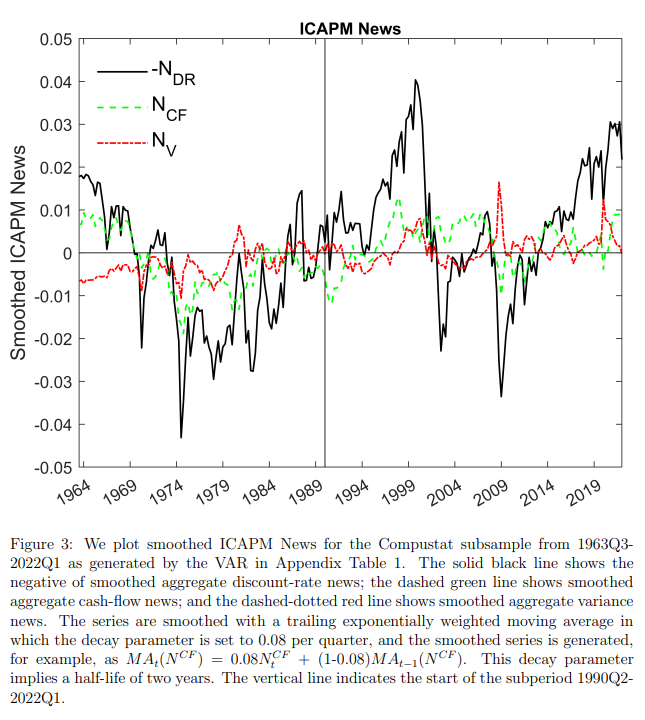

以下は3つのニュースの動きを示した図。

以下は業種間よりも業種内の要素の方がICAPMで上手く説明できることを示した図。

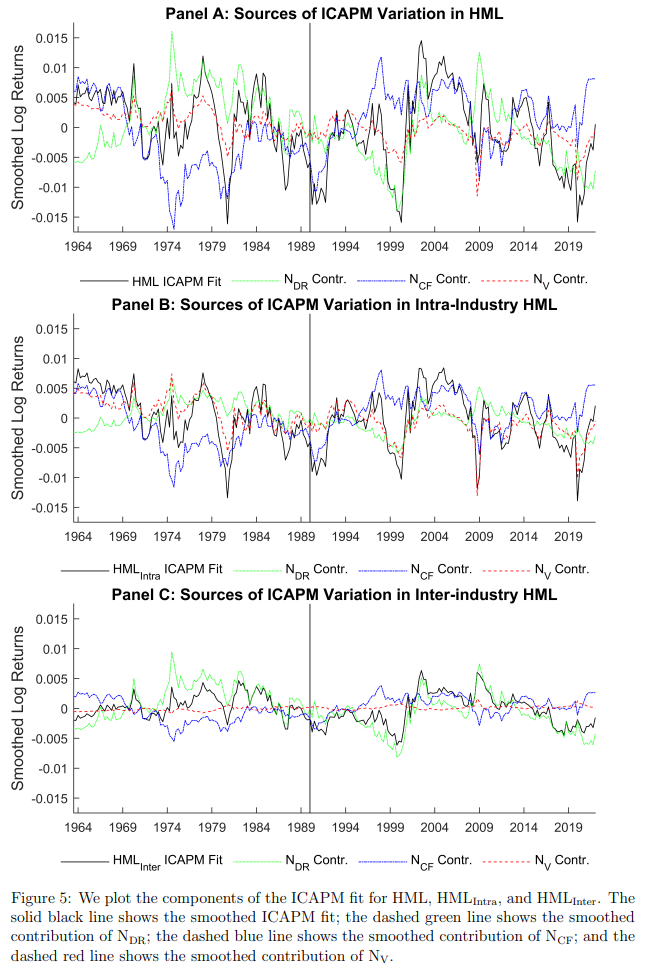

以下はそのICAPMのフィットをさらに3つのショック要因で分解した図。