プリンストン大のマーカス・ブルナーメイヤー(Markus K. Brunnermeier)とユリ・サニコフ(Yuliy Sannikov)のコンビ*1が、もう一人のプリンストン大の研究者Sebastian A. Merkelと共に、表題の件を分析したNBER論文「The Fiscal Theory of Price Level with a Bubble」を上げている(ungated版)。

以下はungated版の導入部の冒頭。

Different monetary theories emphasize different roles of money and different equilibrium equations to determine the price level. The Fiscal Theory of the Price Level (FTPL) stresses the role of money as a store of value and argues that the real value of all outstanding government debt, i.e., the nominal debt level divided by the price level, is given by the discounted stream of future primary government surpluses. Primary surpluses are the difference between government revenue and expenditures excluding interest payments. Absent government default, an increase in primary deficits leads to an increase in the price level, i.e., inflation, by devaluing outstanding debt.

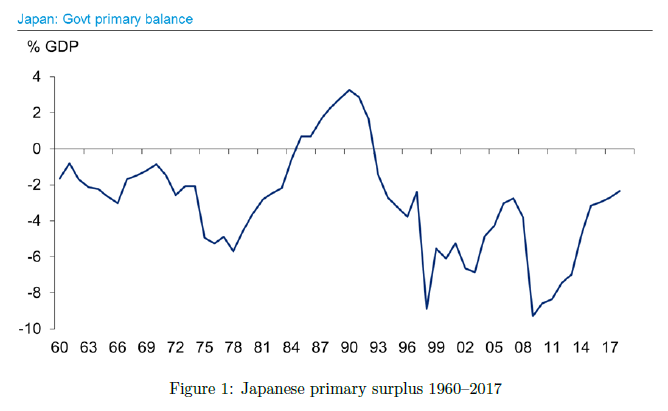

Critics of the FTPL often point to Japan. Even though Japan has mostly run primary deficits since the 1960s (see Figure 1) and with no primary surpluses in sight, the price level has not risen much. Indeed, inflation levels are depressed even though the government and central banks leave no stone unturned to boost inflation closer to 2%.

In this paper, we revisit the key FTPL equation and argue that including the typically ignored bubble term allows us to reconcile the FTPL with Japan's experience. Indeed, we show that the transversality condition is often insufficient to rule out a bubble on the aggregate economy, refuting the usual justification to simply dismiss the bubble term. While the FTPL literature puts a lot of emphasis on distinguishing between monetary and fiscal dominance, the bubble term cannot be ignored under any policy regime.

(拙訳)

相異なる金融理論は、貨幣の相異なる役割と、物価水準を決定する相異なる均衡方程式に力点を置く。物価水準の財政理論(FTPL)は、価値の貯蔵手段としての貨幣の役割に力点を置き、市中の全政府債務の実質価値、即ち名目債務水準を物価水準で割ったものは、将来の基礎的財政黒字の流列を割り引いたものとなる、と主張する。基礎的財政黒字は政府歳入と利払いを除く歳出との差である。政府の債務不履行が無ければ、基礎的財政赤字の増加は、市中の債務の減価を通じて物価水準の上昇、即ちインフレにつながる。

FTPLの批判者は良く日本を例に挙げる。日本は1960年代以降概ね基礎的財政赤字を計上してきており(図1参照)、基礎的財政黒字を近く達成する見込みも乏しいが、物価水準はあまり上昇してない。実際のところ、政府と中銀がインフレを2%近くまで引き上げようとあらゆる手を尽くしているにも拘らず、インフレ水準は抑えられたままとなっている。

本稿で我々は、FTPLの中心的な方程式を再検討し、通常無視されるバブル項を含めることによってFTPLを日本の実例と整合させることができる、と論じる。実際のところ、バブル項を単に除外することを正当化する通常の議論に反駁する形で、横断条件はマクロ経済からバブル項を取り除くには不十分であることが多い、ということを我々は示す。FTPLの研究では金融支配と財政支配の区別を大きく強調するが、いかなる政策体制下でもバブル項を無視することはできない。

導入部では続けてバブル項の出現条件に付いて説明している。バブル項はr ≤ gの時に生じ、そこでの安全利子率rは、リスクプレミアム込みの民間の金利(>g)よりは低くなる、との由。

A bubble term emerges whenever the real rate paid on government debt is persistently below the growth rate of the economy, i.e., whenever r ≤ g. It is well known that this can be the case in overlapping generations models (Samuelson 1958), models of perpetual youth (Blanchard 1985), and incomplete market models a la Bewley (1980). In this paper we provide another simple example based on Brunnermeier and Sannikov (2016a,b) in which the r ≤ g outcome arises naturally and agents can invest in both physical capital and government bonds. Physical capital is subject to uninsurable idiosyncratic return risk. Hence, the expected return on capital exceeds the growth rate g since agents require a risk premium. Government bonds are the safe asset in the economy and allow agents to indirectly share part of their idiosyncratic risk. High idiosyncratic risk makes the government bond more attractive and depresses r below g.

(拙訳)

バブル項は、政務債務の実質金利が恒常的に経済の成長率を下回る時、即ち r ≤ gの時に常に現れる。世代重複モデル(サミュエルソン、1958*2)、不老モデル(ブランシャール、1985*3)、およびビューリー流の不完全市場モデル(1980*4)でそうしたことが成立し得ることは良く知られている。本稿で我々は、ブルナーメイヤーとサニコフ(2016a,b*5)に基づく、r ≤ gの結果が自然に生じるとともに経済主体が物的資本と国債の両方に投資できる別の単純な例を提示する。物的資本には保険が掛けられない固有の収益リスクがある。従って、経済主体がリスクプレミアムを要求することから、資本の期待リターンは成長率gを上回る。国債は経済において安全資産であり、経済主体はそれによって各自固有のリスクの一部を間接的に分散することができる。高い固有リスクは国債をより魅力的なものとし、rをg以下に抑える。

政府は「バブルのマイニング」を行うことによって増税無しに歳出を増やせるとのことである。

By "printing" bonds at a faster rate, the government imposes an inflation tax that reduces the return on the bonds further. Since government bonds are a bubble, the government in a sense "mines a bubble" to generate seigniorage revenue. The resulting seigniorage revenue can be used to finance government expenditures without ever having to raise extra taxes.

For example, if the primary surpluses are always negative, then their discounted stream is also negative, and only the positive value of the bubble can ensure a positive price level. The size of the bubble, and hence the price level, is determined by wealth effects and goods market clearing. A larger bubble raises agents' wealth and hence their demand for output. To ensure goods market clearing, the bubble has to take on a certain size, which together with the FTPL equation determines the price level.

The price level is uniquely determined if the fiscal authority backs the bubble to rule out equilibria that lead to hyperinflation. Such fiscal backing is only required off-equilibrium.

(拙訳)

国債をより速く「刷る」ことで、政府は国債のリターンを一層減じるインフレ税を課すことができる。国債はバブルなので、そのような政府は、ある意味において、シニョリッジ収益を生成するために「バブルの採掘」を行っている。そうして得られたシニョリッジ収益は、追加的な増税を一切行う必要なしに政府歳出を賄うために使うことができる。

例えば、基礎的財政収支が常にマイナスの場合、その割引流列もマイナスとなり、バブルの正の値だけが正の物価水準を保証できる。バブルの大きさ、ひいては物価水準の高さは、資産効果と財市場の清算によって決まる。バブルが大きいと経済主体の富も大きくなり、彼らの生産への需要も高まる。財市場の清算を保証するため、バブルはある程度の大きさになる必要があり、それがFTPL方程式と共に物価水準を決定する。

ハイパーインフレにつながる均衡を取り除くように財政当局がバブルを裏書きすれば、物価水準は一意に定まる。そうした財政による裏書きは均衡の外で行うことが要求される。

最後の段落は意味が取りにくいが、本文の該当の節を見ると、均衡経路では政府は債務を好きな一定の伸び率で伸ばして良いが、債務価値がある閾値を下回ったら、生産に一定税率を課して基礎的財政黒字を確保する、という均衡経路外の操作を行う必要がある(さもないと政府の債務価値が漸近的にゼロに収束してしまう)、ということのようである(その際、そうした均衡外の操作を実施するという公約の信頼性と実現可能性が問題になるが、それは本稿の範囲を超えた話、と断っている)。

また、本文では、シニョリッジを以下の3種類に分類している。