David Andolfattoが失業率とインフレの関係について論じたエントリに、クルーグマンが、インフレが失業率と無関係に貨幣の需給だけで決まると主張している、と噛み付いた。それに対しAndolfattoが、そうではない、フィリップス曲線の話と貨幣の需給の話は相補的なものだというのが本意だ、と反論している。

以下はクルーグマンのエントリからの引用。

Oh, dear. We’ve been here before.

Look, economics is about what people (and businesses – corporations are people, my friends) do. Whatever you think is the ultimate cause of an economic phenomenon, your story about how that phenomenon happens has to include an explanation of how peoples’ incentives change. That’s why the doctrine of immaculate transfer, which asserts that saving-investment balances translate into trade balances without any adjustment of the exchange rate, is silly: producers and consumers don’t know or care about S-I, they need to be induced to change their behavior, which requires a change in relative prices.

Similarly, even if you think that inflation is fundamentally a monetary phenomenon (which you shouldn’t, as I’ll explain in a minute), wage- and price-setters don’t care about money demand; they care about their own ability or lack thereof to charge more, which has to – has to – involve the amount of slack in the economy. As Karl Smith pointed out a decade ago, the doctrine of immaculate inflation, in which money translates directly into inflation – a doctrine that was invoked to predict inflationary consequences from Fed easing despite a depressed economy – makes no sense.

...

And to get back to my broader point: economics is about what people do, and stories about macrobehavior should always include an explanation of the micromotives that make people change what they do. This isn’t the same thing as saying that we must have “microfoundations” in the sense that everyone is maximizing; often people don’t, and a lot of sensible economics involves just accepting some limits to maximization. But incentives and motives are still key.

And it’s ironic that macroeconomists who are deeply committed to the microfoundations project – or, as Trump might say, the “failing microfoundations project” – also seem to be especially likely, perhaps due to their addiction to mathiness, to forget this essential rule.

(拙訳)

あれまあ。この議論は以前にしたものなのだが*1。

ええと、経済学は人々(と企業――企業は人々なのだよ、友よ)の行動に関するものなのだよ。経済現象の究極の原因が何であると思うにせよ、その現象の生起に関する話には、人々のインセンティブがどのように変化するかについての説明が含まれていなくてはならない。貯蓄投資バランスが為替相場の調整を一切抜きにして貿易収支に反映されるという無垢な移転理論*2が馬鹿げているのはそれが理由だ。生産者も消費者も貯蓄投資バランスのことは知らないし気にもかけないが、彼らは行動を変えるように仕向けられる必要があり、そのためには相対価格が変化する必要がある。

同様に、たとえインフレが根本的には貨幣的現象だと考えているにしても(すぐに説明するように、そう考えるべきではないが)、賃金や価格の設定者は貨幣需要のことは気にしていない。彼らはもっと課金できるか否かに関心があるのであり、それは必然的に――必然的にだ――経済にどの程度遊びが存在するかに関係する。10年前にカール・スミスが指摘したように、貨幣が直接的にインフレに反映されるという無垢なインフレ理論――FRBの緩和政策により不況下でもインフレが起きると予測するために持ち出された理論――には意味が無い。

・・・

全般的な話に戻ると、経済は人々の行動に関する話であり、マクロの行動に関する話には、人々がなぜ行動を変えたかというミクロの動機に関する説明が必ず含まれていなくてはならない。これは、皆が最大化を行うという「ミクロ的基礎付け」が無くてはならない、という話とは違う。人々が最大化を行わないことは良くあり、多くの分別ある経済学は最大化に何らかの限界があることをとにかく受け入れている。とは言え、インセンティブと動機は依然として重要である。

ミクロ的基礎付けプロジェクト――トランプの言を借りれば、「失敗しつつあるミクロ的基礎付けプロジェクト」――に深く献身しているマクロ経済学者が、おそらくは数学っぽさに耽溺するあまり、この基本ルールをどうやら忘れたらしい、というのは皮肉なことだ。

このようにクルーグマンはAndolfattoに対してかなり揶揄的な言葉遣いをしているが、対する応答エントリでAndolfattoは、かつてクルーグマンを遠慮会釈なしに罵倒していた氏に似合わず、意外にも丁寧な言葉遣いに徹している*3。

クルーグマンはエントリの冒頭で以下の3つの問いを立てているが、

Andolfattoは1番目と2番目の点についてはクルーグマンに同意する、と述べている。即ちFRBは失業率がどこまで下がるか知らないという点でクルーグマンに同意し、引き締めに関しては次のように書いている。

This is legitimately debatable--and the FOMC is presently debating it. My own view, on balance, seems presently more aligned with the "doves" on the committee. And so I also agree with Krugman on this score, namely, that the Fed could be tightening too aggressively. Krugman suggests that there are several reasons supporting his view and he mentions a few of them. They are all legitimate reasons, in my view. But I could add more reasons, based on my own preferred theory of inflation. The demand for money (broadly defined to include U.S. treasuries) appears to remain elevated. This disinflationary force has been in place for a long time and could, as I explain here, account for the lowflation phenomenon (see also here). If you follow that link, you'll note that I quote Krugman approvingly in regard to his view about monetary policy in a liquidity trap. Perhaps I am wrong, but I read Krugman here as not recommending that the Japanese lower their unemployment rate to raise inflation. Instead, he appeals to the model I alluded to in my post: a monetary-fiscal theory of inflation. If the Japanese want inflation, just cut taxes and finance social security spending by printing JGBs (as I recommended here). I'm not sure what this has to do with "immaculate" inflation. (I did learn from Nick Rowe that "maculate" is indeed a word.)

(拙訳)

これはまともな議論でも意見の分かれるところであり、FOMCでも議論が続いている。私自身の見解は、全体的に言えば、今はFOMCの「ハト派」に近いかと思われる。ということは、この点ではクルーグマンとも意見が同じ、ということである。即ち、FRBは引き締めに積極的過ぎるかもしれない、と考えている。クルーグマンは自分の見解を裏付ける理由は複数あると述べており、そのうちの幾つかに言及している*4。私に言わせればそれらはすべて正当な理由であるが、私のお気に入りのインフレ理論からさらなる理由を付け加えることができる。貨幣(米国債を含む広義の貨幣)への需要は、高まったままのように思われる。このディスインフレ的な力は長期間存在しており、ここで解説したように、低インフレ現象を説明することができる(ここも参照)。リンクを辿れば、流動性の罠における金融政策について私がクルーグマンの見解を肯定的に引用していることに気付くだろう。私が読み間違えているのでなければ、ここ*5でクルーグマンが提唱しているのは、インフレを上昇させるために失業率を下げることではない。クルーグマンは、私が記事で触れたモデル、即ちインフレの金融財政理論に訴求している。もし日本がインフレを欲しているのであれば、減税を行って社会保障支出を国債を発行して賄えば良い(それは私がここで推奨したことである*6)。それと「無垢な(immaculate)」インフレがどのように関係しているのかは私には良く分からない(「maculate」という言葉があることはNick Roweに教えて貰ったが)。

そして、3番目の点については以下のように書いている。

I think it would be odd for any macroeconomist schooled in general equilibrium to suggest that the answer to this question is unequivocally no. The answer is yes. The real question is what type of relationship? ...

So perhaps there's some room for debate on point 3. But we should be careful not portray the question as an "either/or" issue. We could just be two blind men, feeling different parts of the elephant--the two interpretations are not necessarily inconsistent with each other. We should try to work this out. On the plus side, it seems we are led to the same policy recommendation. This is something worth noting. (I plead guilty on the score of needlessly antagonizing people who "believe in" the Phillips curve. Rather than suggesting we abandon the theory, I could instead have suggested we supplement it with the monetary view.)

Does the debate over question 3 matter? Yes, it could, because different interpretations of how the world works usually--though not always---implies something different about optimal policy. The Phillips curve theory of inflation suffers from a free parameter problem: the natural rate is unobservable and hence, one can always appeal to a shift in the natural rate to explain away discrepancies with the data. However, the monetary theory I prefer also suffers from a free parameter problem: money demand is not directly observable either. I can always appeal to some unobserved shift in money demand to explain away discrepancies with the data. For this reason, it would be useful for economists to identify "robust" policies--policies that can be expected to deliver good results regardless of which theory best describes the world we are living in.

Is the Phillips curve view of inflation contributing to a policy mistake? I wanted to suggest in my post that it is, although this is not necessarily a fault of the theory as much as how it is applied. That is, there may be no policy mistake in the making if the FOMC simply lets its estimate of the natural rate fall freely as evidence of impending inflation fails to materialize. However, this is not what is happening. As Jim Bullard explained to me, he believes that Phillips curve proponents have a (strictly positive) lower bound on their estimate of the natural rate. The unemployment rate is so low now -- how can it possibly go any lower -- this has to lead to inflation in the near future -- it just has to. We'd better start raising now, before we find ourselves behind the curve.

Here is where the "monetarist" view could temper such resolve. Granted, the global outlook is looking relatively rosy, and fiscal policy seems expansionary--these are both inflation risks from a monetarist perspective. On the other hand, there is considerable uncertainty in this outlook, not the least of which is presently being fueled by talk of a global trade war. In uncertain times, consumers and investors are likely to lower their demand for goods and services--increasing their demand for safe assets, like U.S. dollars and U.S. treasuries. We can see these concerns weigh on long-bond yields. Market-based inflation expectations (like the 5yr-5yr forward) seem well-anchored. Current inflation is running below target. All of this suggests that the Fed can afford not to move aggressively at this time (to be fair, the FOMC regularly emphasizes the "data dependent" nature of its policy path). And yes, this is consistent with PC advocates that are willing to let their estimate of the NRU decline in line with the evidence.

(拙訳)

一般均衡の学派に属するマクロ経済学者が、この問いへの回答は明らかに否である、などと言うのは変だと思う。回答はイエスである。真の問題は、どんな関係か、ということにある。・・・

ということで、3点目については議論の余地があるかもしれない。しかしこの問いを二者択一問題として捉えないように注意する必要がある。我々は象の異なる部分を手探りしている2人の盲人に過ぎないのかもしれず、2つの解釈は必ずしも互いに矛盾しているとは限らない。我々は解明に努めるべきなのだ。プラスの面としては、我々は同じ政策提言に辿り着いているように思われる。これは注目に値することである(フィリップス曲線を「信じる」人の反感を不必要に買った、という点では私は罪を認める。理論を棄却することを提唱するのではなく、金融的な見方で補完することを提唱すべきだった)。

問3を巡る議論は重要だろうか? イエス、重要なものとなり得る。というのは、世界がどのように動いているか、についての異なる解釈は、最適政策についての含意が異なることが多い――常に異なるわけではないが――からである。インフレのフィリップス曲線理論には、自由パラメータ問題がある。即ち、自然失業率は観測不可能であるため、データとの乖離を自然失業率の変化で片付けることが常に可能である。しかし、私の好きな貨幣理論にも自由パラメータ問題がある。貨幣需要というのも直接に観測可能ではないからだ。データとの乖離を観測できない貨幣需要の何らかの変化で片付けることが常に可能である。以上の理由から、「頑健な」政策を識別することが経済学者にとって有用である。それは、我々の住む世界をどの理論が最も良く描写するかとは無関係に、良い結果をもたらすことが期待できる政策である。

インフレのフィリップス曲線的な見解は、政策の過ちに寄与しただろうか? 私の最初の記事で示したかったのは、そうした寄与があった、ということである。ただし、それは必ずしも理論の問題ではなく、その適用の仕方の問題だった。即ち、インフレが差し迫っている証拠が顕在化しないことから、自然失業率の推計値が低下するに任せていれば、FOMCの政策策定の過ちは生じないであろう。だが、実際にはそうなっていない。ジム・ブラードが私に説明してくれたのだが、彼の考えでは、フィリップス曲線の主唱者は、自然失業率の推計に際して(ゼロより大きい)下限を設けている。今や失業率はこれだけ低いのだから――これ以上低くなりようがあろうか――近い将来にインフレが生じるに違いない、それは間違いなく生じる、というわけだ。そこから、手遅れになる前に利上げを今始めよう、ということになる。

ここで、そうした思い込みを軟化させる「マネタリスト」的見解の出番である。確かに、世界経済は比較的見通しが明るく、財政政策は拡張的なように思われる。これらはいずれもマネタリスト的見解からすればインフレリスクである。その一方で、この見通しには顕著な不確実性が存在し、現状では貿易戦争の話が少なからずその不確実性を上昇させている。不確実な時期には、消費者と投資家は財やサービスへの需要を減らし、米ドルや米国債などの安全資産への需要を増やす可能性が高い。我々は長期債利回りにこの懸念が反映されているのを見ることができる。市場ベースのインフレ期待(5年先の5年先フォワードなど)はかなり安定しているように思われる。現在のインフレは目標を下回っている。以上のことはすべて、FRBが現時点で積極的に動く必要は無い、ということを示唆している(公平を期すならば、FOMCは政策経路の「データ依存的」な性格を常に強調している)。そして、そう、これは、自然失業率の推計値を証拠に沿って低下させる意思のあるフィリップス曲線の主唱者の考えと整合的である。

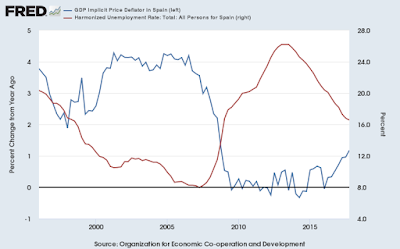

なお、インフレが根本的には貨幣的現象だと考るべきではなく、インフレと失業率には関係がある、という点についてクルーグマンは、スペインのデータを証拠として挙げていた。即ち、ユーロに参加したことによりスペインには独自の金融政策が無かったが、危機前のインフレの高い時期に失業率は低く、危機後のインフレの低い時期に失業率は高かった(下図)。

それに対しAndolfattoは、公債を含む貨幣への需要ショックがこうした振れを引き起こした、という解釈を示している。また、データからは低失業率が高インフレを予測したようにも読めるが、そうしたナイーブな解釈は注意を要する、というのが最初のエントリの主旨だった、とも述べている。

最後にAndolfattoは、クルーグマンの「経済は人々の行動に関する話であり、…インセンティブと動機は依然として重要である」という箇所に全面的に同意する、と述べてエントリを締め括っている。

*3:それで気付いたが、彼は差し障りのありそうなエントリをいつの間にか軒並み削除している(例:本ブログのここ、ここ、ここ[の追記]、ここ、ここ、ここ、ここ、ここでリンクしていたエントリ。中には3/16付けのグーグルキャッシュが残っているものもあるので、少なくとも一部はかなり最近削除したらしい)。7年前に別件で炎上騒ぎを経験した後も歯に衣着せぬブログ活動を続けていた彼だが、セントルイス連銀勤めが今年10年目に入ることもあり、かつてタッグを組んでクルーグマンやデロングの悪口を言っていたStephen Williamson(eg. ここ)とは対照的に、大人になったようだ。あるいはWilliamsonが2014年から勤務していたセントルイス連銀を昨年退職したことと考え合わせて下衆の勘繰りをするならば、ブラード総裁辺りから何らかのお達しがあったのかもしれない…。

*4:具体的には、失業率がどこまで低下するか分からないこと、間違えた場合の対価が非対称的であること(引き締めが遅すぎるのはバツが悪いかもしれないが、早過ぎるのは流動性の罠に戻るリスクを高める)、2%のインフレ目標は低過ぎる(それでゼロ金利下限を回避するのには十分、という考えは各所での経験により完全に粉砕された)、という点をクルーグマンは挙げている。