10/6エントリで触れた、ECB ForumでのCharles Goodhartの発言を要約した元IMFエコノミストのChris Marshのツイートを紹介しておく。

Then came Goodhart who we will now quote at length:

“The world at the moment is in really a rather extraordinary state because we have no General Theory of Inflation. We used to have two inter-connected theories. One of these was the Friedman monetary theory that inflation is always and everywhere a function of too much money...

"chasing too few goods.

Now that theory has become so discredited that central banks now as a general matter do not even mention monetary aggregates at all and seem embarrassed to do so. [Aside: not strictly true of the ECB, though downplayed since the Strategy Review.]

"Then of course there is the somewhat inter-connected Phillips Curve, the relationship between the natural level of unemployment and the rate of inflation. And that has also been behaving rather oddly.

"So, into this vacuum has come what I rather tend to consider as 'the bootstrap theory of inflation,' which is that as long as inflation expectations are anchored, inflation will also remain anchored.

"In other words that inflation depends on its expectations. Now this unfortunately is a very weak reed. It’s a very weak read because actual inflation expectations are much more closely associated …

with what has happened in the past, which people tend to extrapolate, than what is likely to happen in future.”

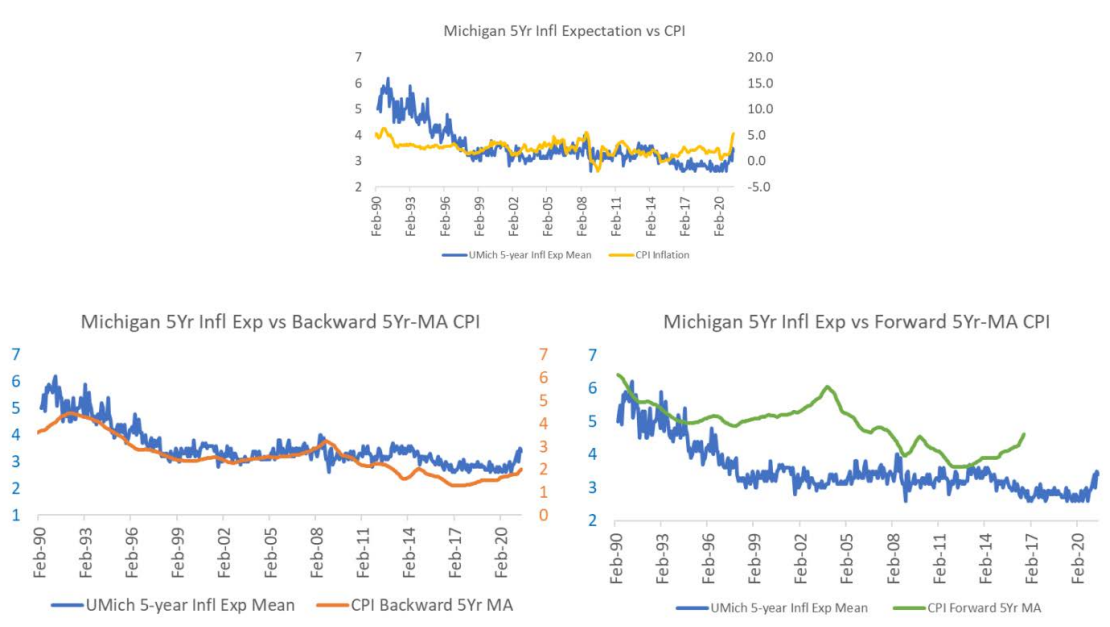

Goodhart then showed a chart of how the Michigan 5Y inflation expectations in the US are more a function of past than prospective inflation out turns. He continued...

“So that inflationary expectations are really not very good and not very useful in indicating what is likely to happen in future. They are adaptive and backwards looking.”

Goodhart then goes on to reference (and read from) the Rudd staff paper at the Federal Reserve last week.

Now it is a remarkable intervention from a respected senior member of the profession and former Bank of England MPC member, though entirely true, that the macroeconomics does not have a General Theory of Inflation.

(拙訳)

次にグッドハートが登壇した。少し長くなるが引用する:

「インフレの一般理論が存在しないことで、現在の世界はかなり異常な状況にあります。かつては2つの相互に関連する理論がありました。一つはフリードマンの貨幣理論で、インフレはいつでもどこでも多すぎる貨幣が少なすぎる財を追うことの作用である、というものでした。

今やその理論はあまりにも信頼を失ったので、一般的に現在の中銀は貨幣集計量に全く言及さえしませんし、そうすることを恥じているように見えます[注記:ECBについてはそれは厳密には正しくないものの、戦略レビュー以降は控えめになっている]。

それからもちろん、それと幾ばくか相互関連しているフィリップス曲線があります。失業率の自然水準とインフレ率の関係です。それもかなり奇妙な振る舞いを見せてきています。

この空白を突いて、私に言わせれば「インフレのブートストラップ理論」なるものが現れました。インフレ予想が固定されている限り、インフレも固定される、というものです。

言い換えれば、インフレはその予想に左右されるというわけです。残念ながらこれは非常に貧弱な枠組みです。というのは、現実のインフレ予想は、将来起きそうなことよりも、人々が外挿しがちな過去に起きたこととより密接に結び付いているからです。」

グッドハートはそれから、ミシガンの米国5年インフレ予想が、その先のインフレの実際の結果よりもむしろ過去のインフレの関数であることを示すチャートを提示した*1。彼は続けて以下のように述べた。

「ということで、インフレ予想は将来に起きそうなことを示す上であまり良い指標ではなく、あまり役に立ちません。それは適応的で、バックワードルッキングなのです。」

それからグッドハートは、先週のラッドのFRB研究員論文を参照(かつそこから引用)した。

マクロ経済学にはインフレの一般理論がない、というのは、完全に真実ではあるが、イングランド銀行金融政策委員も務めた学界の尊敬されるベテランからの注目すべき発言である。

ちなみにMarshはこの引用の前で、同じセミナーの講演でIMFチーフエコノミストのギータ・ゴピナートが提示したIMFのインフレ予測を、グッドハートの批判を先取りして体現したようなもの、とこき下ろしている。Marshの見解では、IMFのユーロ圏のインフレ予測は、ECBが市場の予想を操作しようとして2%以下の予測を提示してきたのに考えなしに倣ったものである。かつてユーロ危機時に経常収支/国内需要調整とその後のディスインフレを予測し損ねたのと同様に、IMFは、現れつつあるインフレ圧力を認識するのが遅れている可能性が高い、とMarshは言う。その上で、国内の経済政策でIMFのお墨付きに依存するのは、処方箋をハロルド・シップマンに依存するようなもの、とまで批判している。

またMarshは、上記の引用の後で、マクロ経済学には有効需要の一般理論もない、と述べている。そしてその問題が生じた主要な原因として、クルーグマンの「It's Baaack」論文と、エガートソン=ウッドフォードの「The Zero Bound on Interest Rates and Optimal Monetary Policy」論文を槍玉に挙げている。Marshに言わせれば、異時点間の枠組みを使って現在の問題を将来の行動で解決しようとするのは、所得の配分、資金の流れ、金融構造といった現時点の問題を蔑ろにするものであり、政策当局者の現時点の不作為を正当化するもの、とのことである。そうした枠組みでは予想が重要な役割を果たすが、グッドハートが指摘したように、予想は実際には過去の関数であるため、それに基づく政策は過ちを犯すことになる、とMarshは警告している。