というNBER論文が上がっている(ungated版)。原題は「The Race Between Asset Supply and Asset Demand」で、著者はAdrien Auclert(スタンフォード大)、Hannes Malmberg(ミネソタ大)、Matthew Rognlie(ノースウエスタン大)、Ludwig Straub(ハーバード大)。

以下はその要旨。

We introduce an asset supply-and-demand approach to analyze the trajectory of US aggregate wealth, real interest rates, and fiscal sustainability. Our framework uses micro-founded and easy-to-implement sufficient statistics to quantify how shifts in demographics, inequality, and other forces affect asset market equilibrium. From 1950 to the present, rapid population aging, rising income inequality, increasing foreign demand for US assets, and declining productivity growth all contributed to a surge in asset demand. Asset supply initially fell, then turned around sharply, mainly driven by increases in government debt and the value of capitalized profits. Overall, asset demand won the race, and interest rates fell. Looking ahead to 2100, population aging will continue to strongly push up asset demand, but at current tax and benefit levels, asset supply will win the race, as rising entitlement costs push up government debt even more. While rising asset demand creates space for debt to eventually reach 250% of GDP without higher interest rates, stabilizing debt at any level requires a permanent fiscal adjustment of at least 10% of GDP.

(拙訳)

我々は、米国の総資産、実質金利、および財政の持続可能性の経路を分析するために資産の需給アプローチを導入する。我々の枠組みは、ミクロの基礎付けがあり実装が容易な十分統計量を用いて、人口動態、格差、およびその他の力の変化がどのように資産市場の均衡に影響するかを定量化する。1950年から現在まで、急速な人口の高齢化、所得格差の拡大、米国資産への海外需要の増加、および生産性成長率の低下がすべて資産需要の急伸に寄与した。資産供給は当初は低下し、その後、政府債務と資本化された利益の価値の増加を主因として急速な上昇に転じた。総じて、資産需要が競争に勝ち、金利は低下した。2100年までの見通しでは、人口の高齢化が引き続き資産需要を強く押し上げるが、現在の税の給付の水準では、上昇する給付費用が政府債務をさらに押し上げるため、資産供給が競争に勝利する。資産需要の増加は、金利を上昇させることなしに債務が最終的にGDPの250%に達する余地を生み出すが、どの水準であっても債務を安定化させるためには、少なくともGDPの10%の恒久的な税制調整が必要となる。

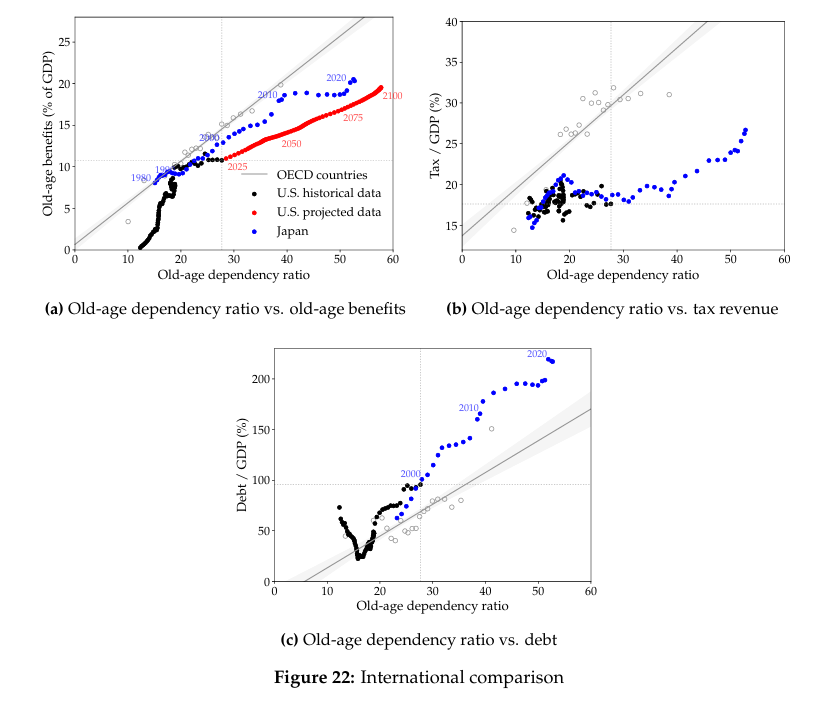

論文では、以下の図を掲げ、パネル(a)の高齢者の依存人口比率と高齢者への給付の関係について、今後75年の米国の軌跡は、今世紀に入ってからの日本と似たようなものになるだろう、としている。またパネル(b)について、高齢化に対応する日本の税調整は遅れた、としている。パネル(c)については、日本は高齢化が債務水準の上昇をもたらした典型例、としている。