というNBER論文が上がっている(ungated版)。原題は「Quantities and Covered-Interest Parity」で、著者はTobias J. Moskowitz(イェール大)、Chase P. Ross(FRB)、Sharon Y. Ross(同)、Kaushik Vasudevan(パデュー大)。

以下はその要旨。

Studies of intermediated arbitrage argue that bank balance sheets are an important consideration, yet little evidence exists on banks’ positioning in this context. Using confidential supervisory data (covering $25 trillion in daily notional exposures) we examine banks’ positions in connection with covered-interest parity (CIP) deviations. Exploiting cross-sectional variation in CIP deviations that have largely challenged existing theories, we document three novel forces that drive bases: 1) foreign safe asset scarcity, 2) market power and segmentation of banks specializing in different markets, and 3) concentration of demand. Our findings shed empirical light on the interplay of frictions influencing banks’ provision of dollar funding.

(拙訳)

仲介機関経由の裁定についての研究は、銀行のバランスシートが考慮対象として重要であると論じているが、この文脈における銀行のポジションについては実証結果がほとんどない。内密の監督データ(日次の名目エクスポージャーの25兆ドルをカバーしている)を用いて我々は、カバー付き金利平価(CIP)からの乖離との関連において銀行のポジションを調べた。既存の理論から大きく外れているCIPからの乖離の横断面におけるバラツキを利用して我々は、ベースを動かす3つの新たな力を明らかにした。1) 海外の安全資産の稀少性、2) 市場支配力と、相異なる市場に特化している銀行の細分化、および、3) 需要の集中、である。我々の発見は、銀行のドル調達の供給に影響する摩擦の相互作用に実証的な解明の光を投じる。

以下は本文の冒頭。

Spreads on bank-intermediated arbitrage trades, called bases, have persisted since the 2008 financial crisis, attracting substantial attention from academics and practitioners. The existence of bases is often cited as evidence that financial intermediaries are not simply a veil, as assumed in classical theories.

(拙訳)

銀行が仲介する裁定取引におけるスプレッドは、ベースと呼ばれるが、2008年の金融危機以降継続しており、学界と実務者から大いに注目を集めている。ベースの存在は、金融仲介者が古典理論で仮定されているような単なるヴェールではない証拠として引用されることが多い。

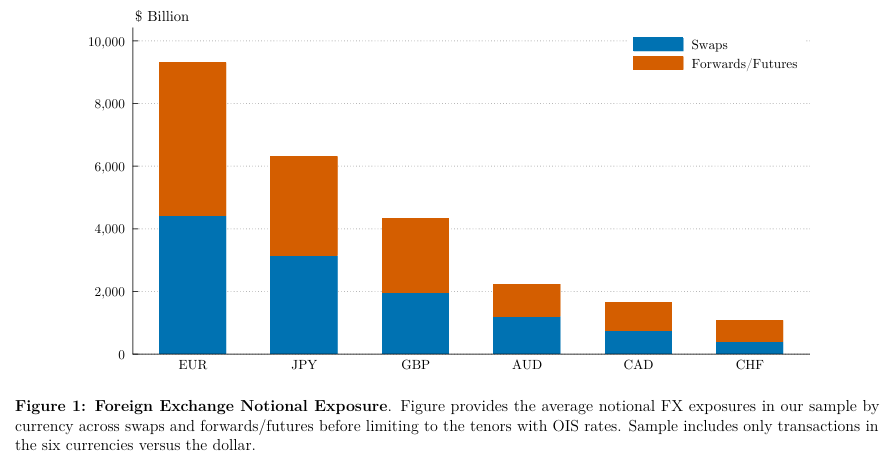

以下は研究対象とした為替デリバティブの名目エクスポージャーを表したグラフ。

CIPからの乖離を取り上げたという点ではドル不足、CIPからの乖離、およびドルの避難先としての役割 - himaginary’s diaryで紹介した研究に近いようにも見えるが、そちらの研究のようなマクロ的な観点からではなく、ミクロ的な仲介機関の役割という観点から解明を試みたことがこの研究の特徴と言えそうである。