というNBER論文が上がっている(ungated版)。原題は「Inflation and Treasury Convenience」で、著者はAnna Cieslak(デューク大)、Wenhao Li(南カリフォルニア大)、Carolin Pflueger(シカゴ大)。

以下はその要旨。

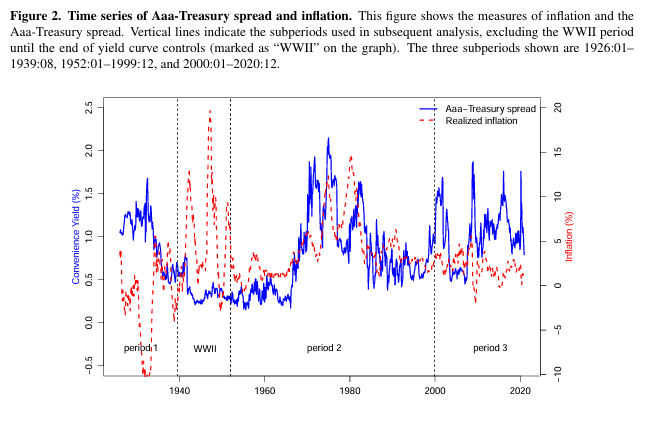

Using a century of data, we show that Treasury convenience yield and inflation comove positively during the inflationary 1970s-1980s, but negatively pre-WWII and post-2000. An inflation decomposition reveals that higher supply inflation predicts higher convenience, while lower demand inflation follows higher convenience. In our model, inflationary cost-push shocks raise the opportunity cost of holding money and money-like assets, inducing higher convenience, as in 1970s-1980s. Conversely, liquidity demand shocks drive up convenience but lower consumption demand and inflation in the model, as pre-WWII and post-2000. By linking the evidence to macroeconomic drivers, our results challenge the notion that inflation directly depresses Treasury convenience.

(拙訳)

一世紀のデータを用いて我々は、国債のコンビニエンスイールドとインフレが1970-80年代は正の共変動をしたが、第二次大戦前と2000年以降は負の共変動をしたことを示す。インフレの分解が示すところによれば、供給インフレの上昇はコンビニエンスイールドの上昇を予測し、コンビニエンスイールドの上昇後は需要インフレの低下が生じる。我々のモデルでは、インフレ的なコストプッシュ・ショックは、1970-80年代のように、貨幣と貨幣類似の資産を保有する機会コストを引き上げ、コンビニエンスイールドの上昇を促す。逆に、モデルでは、流動性需要ショックは、第二次大戦前と2000年以降のように、コンビニエンスイールドを押し上げるが、消費需要とインフレを低下させる。実証結果とマクロ経済的な要因を結び付けることにより我々の結果は、インフレが国債のコンビニエンスイールドを直接的に抑制するという考え方に異議を唱える。

以下は実際の推移を示した図。