FRBは引き締めすぎ、という論陣を張っているクルーグマンが、自分の考えをまとめた連ツイを立てている。

A thread on Fed policy, explaining — partly to myself — where I'm coming from. The first thing to say is that in a *qualitative* sense my views are depressingly mainstream. My working model is that inflation, other things equal, reflects unemployment and expected inflation 1/

This model could be wrong! Hoping that @Claudia_Sahm will explain why she wants to ban the Phillips curve (and how to replace it) when we have a CUNY event on the 19th 2/

But if you accept that model, there is at any given time an unemployment rate — u* — at which actual inflation will more or less match expected inflation. (Don't like calling it a NAIRU — with anchored expectations, which we seem to have, u<u* doesn't cause accelerating inf) 3/

This leaves three questions:

1. What is u*?

2. Do we need to go above it?

3. What Fed policy is needed to get where we need to go? 4/

Pre pandemic, u* seemed to be around 3.5, which is where we are now. However, high vacancies and high core inflation seemed to suggest a big rise. However however, vacancies coming down rapidly and wage growth not that high. 5/

Does u need to go well above u*, Volcker style? Some people still saying that, still talking about "sacrifice ratios", but I don't get it. The Volcker slump was an effort to squeeze out high inflation expectations. But expected inflation isn't high now 6/

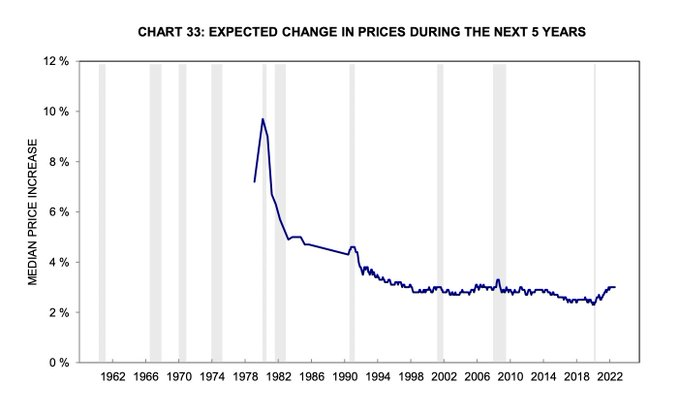

Longer perspective, to show how different things are this time 7/

So I just don't see the case for a period of "excess" unemployment. That still leaves the question of how much more, if any, Fed tightening is required to cool the economy to a sustainable temperature 8/

Personal background may matter here. My macro roots are in international, where we've always known that there are long lags in the effect of exchange rates on trade flows, leading to phenomena like the J-curve 9/

And the strong dollar will in fact exert a major contractionary effect on the US, but not for a number of months yet. The other major channel is through housing. And surely there are significant lags there too 10/

I mean, do you really think we've seen anything like the full effects of the financial tightening that has already happened? 11/

Also good reason to believe that measured inflation will lag well behind economic cooling, if only because of issues involving shelter. 12/

So even given a very mainstream view of how this stuff works, I see a strong case that the Fed has already done enough even if the most recent job numbers were strongish and inflation not yet down. 13/

You want to shoot ahead of a moving target, not behind it 14/

(拙訳)

一つには自分自身の考えをまとめるために、自分の考えの由来について説明するFRBの政策についてのスレッド。まず言っておくべきは、「定量的な」点では私の見方は悲しくなるほど主流派であるということ。私の使っているモデルは、他の条件が等しければ、インフレには失業率と予想インフレが反映される、というものである。

このモデルが間違っている可能性もある! 19日にニューヨーク市立大学で開催するイベントでクラウディア・サームが、彼女がフィリップス曲線を禁止したい理由(とそれをどのように置き換えるか)を説明することを期待しよう。

しかしこのモデルを受け入れるならば、どの時点においても、実際のインフレが予想インフレと曲がりなりにも一致する失業率u*が存在する(これをNAIRUとは呼びたくない――現在そうであると思われるように予想が固定されているならば、u<u*は加速するインフレをもたらさない)。

これにより3つの疑問が生じる。

- u*は何か?

- 失業率はそれより高くなるべきなのか?

- 必要とされる状態に行くためにどのようなFRBの政策が必要とされているのか?

コロナ禍前には、u*は3.5近辺と思われていて、それは現在の失業率の水準である。しかし、高い欠員率と高いコアインフレは、u*が大きく上昇したことを示唆しているように思われた。しかししかし、欠員率は急速に減少しており、賃金の伸びはそれほど高くない。

www.nytimes.com

uはボルカー流にu*よりもかなり上に行かなくてはならないのか? 未だにそう言っている人がいて、未だに「犠牲率」について云々しているが、私には理解できない。ボルカー不況は高いインフレ予想を追い出そうとするものだった。だが今のインフレ予想は高くない。

今回どれだけ状況が違うかを示すため、もっと長期のグラフ。

ということで、「高過ぎる」失業率の期間を正当化する根拠が私には全く理解できない。それでも、経済を持続可能な体温に冷やすためにFRBの引き締めがまだ必要だとして、それがあとどれくらい必要なのか、という問題は残る。

ここで私の個人的背景が効いてくるかもしれない。私のマクロ経済学の原点は国際経済学で、そこでは為替相場が貿易の流量に与える影響には長いラグがあることが以前から知られていた。それによってJカーブ効果のような現象が生じる。

www.investopedia.com

強いドルは実際に米国経済に大きな収縮効果をもたらすだろうが、それが現れるにはまだ何か月か掛かるだろう。他の主要な経路は住宅経由である。そして間違いなくそこにも有意なラグが存在する。

言いたいのは、既に実施された金融引き締めの効果を完全に目にしていると本当に思うのか、ということである。

また、測定されたインフレと経済のクールダウンとの間にはかなりラグがある、と考えるべき理由もある。たとえ住宅サービス関連の問題だけでそうしたラグが生じているとしても、だ。Rents on new leases are falling. Good news, will eventually slow inflation--just don't expect much relief in the official data soon:

— Jason Furman (@jasonfurman) 2022年10月8日

1. The CPI (appropriately) covers ALL leases, not just NEW leases. And existing leases likely re-setting up.

2. The CPI has additional lags. pic.twitter.com/vqHABchlIa

ということで、こうしたことがどのように動くか、についての非常に主流派的な見方を取ったとしても、FRBは既に十分にやった、と言うべき強い根拠があると私は考える。たとえ直近の雇用の数字が強めで、インフレがまだ下がっていないとしても、だ。

我々は動く標的の前方を撃ちたいのであって、後方を撃ちたいわけではないのだ。