ここで紹介したインフレに関する3/18ツイートの補足のようなツイートをクルーグマンが3/28に呟いていたので、以下に紹介しておく。

So, this really is a very tight labor market. Yesterday in New Jersey 1/

But with all the talk about being behind the curve on inflation, I wonder whether people are now getting behind the curve on a likely slowdown in aggregate demand. The real interest rates that matter for investment are rising fast 2/

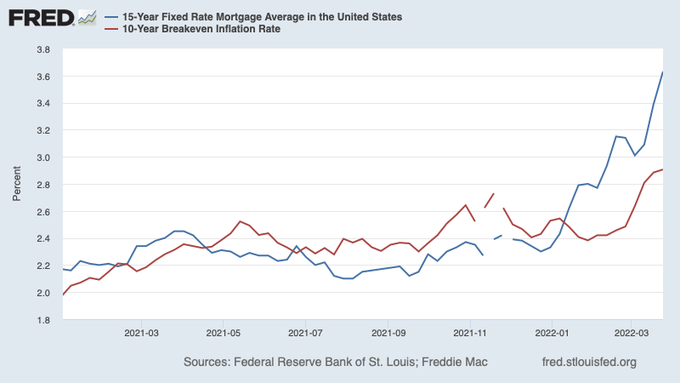

And as I keep arguing, the relevant expected rate of inflation isn't the 10-year rate — it's something like the 10 year 1 year forward, because near-term inflation due to oil and food isn't relevant to investment 3/

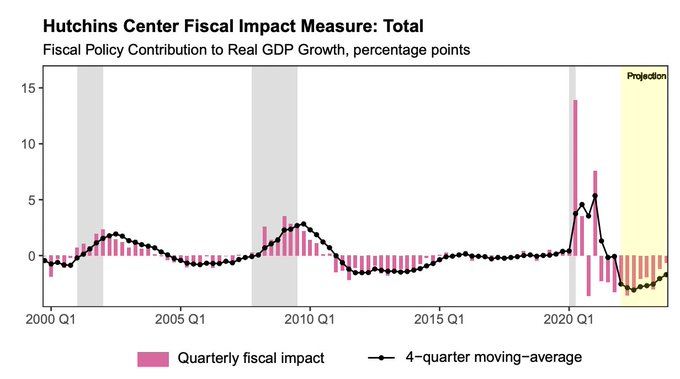

Fiscal policy is turning contractionary 4/

And rising energy and food prices will hit consumer demand for other goods 5/

Seems pretty likely to me that the Fed will be hiking into a significant slowdown. To some extent that's OK — the economy is overheated and needs to cool down. But reason to move gradually 6/

(拙訳)

ということで、労働市場は本当に非常に逼迫している。昨日ニュージャージーにて。

しかし、インフレに後れを取ったという議論がかまびすしいが、これから起きる可能性が高い総需要の鈍化に今は皆が後れを取っているのではないかと思う。投資にとって重要な実質金利は急速に上昇している。

そして私が言い続けているように、重要な予想インフレ率は10年物ではない。1年先の10年物のようなものである。というのは、原油と食料が押し上げる目先のインフレは投資にとって重要ではないからである。I tried to write about the demand side yesterday, but I suspect nobody understood my point. So here's another try 7/ https://t.co/DH4XgwS0o0

— Paul Krugman (@paulkrugman) 2022年3月17日

財政政策は緊縮に転じている。

また、エネルギーと食料価格の上昇は、他の財への消費者への需要に打撃を与える。

今後、景気の著しいスローダウンが生じる中でFRBが金利を引き上げていく可能性が大いにあるように私には思われる。ある程度まではそれはOKだ――経済は過熱しており、クールダウンが必要だ。だが動きを段階的なものにすべき理由にはなっている。