というNBER論文をローレンス・ボールらが上げている。原題は「Measuring U.S. Core Inflation: The Stress Test of COVID-19」で、著者はLaurence M. Ball(ジョンズ・ホプキンス大)、Daniel Leigh(IMF)、Prachi Mishra(同)、Antonio Spilimbergo(同)。

以下はその要旨。

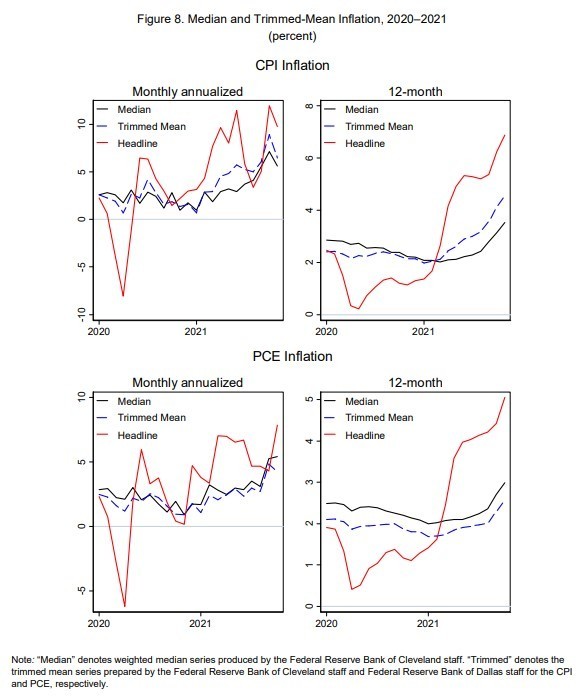

Large price changes in industries affected by the COVID-19 pandemic have caused erratic fluctuations in the U.S. headline inflation rate. This paper compares alternative approaches to filtering out the transitory effects of these industry price changes and measuring the underlying or core level of inflation over 2020-2021. The Federal Reserve’s preferred measure of core, the inflation rate excluding food and energy prices, has performed poorly: over most of 2020-21, it is almost as volatile as headline inflation. Measures of core that exclude a fixed set of additional industries, such as the Atlanta Fed’s sticky-price inflation rate, have been less volatile, but the least volatile have been measures that filter out large price changes in any industry, such as the Cleveland Fed’s median inflation rate and the Dallas Fed’s trimmed mean inflation rate. These core measures have followed smooth paths, drifting down when the economy was weak in 2020 and then rising as the economy has rebounded.

(拙訳)

コロナ禍の影響を受けた業種での大きな価格変化は、米国の総合インフレ率に異常な変動をもたらした。本稿はそれらの業種の価格変化の一時的な影響を除去して2020-2021年の基礎的ないしコアなインフレ水準を測定する代替的な手法を比較する。FRBが好むコアの指標である食料とエネルギーを除くインフレ率は、成績が良くなかった。2020-2021年の大半において、その変動の大きさは総合インフレと同等だった。アトランタ連銀の粘着価格インフレ率のような、固定された業種の集合をさらに除いたコアの指標はより変動が小さかったが、最も変動が小さかったのは、クリーブランド連銀の中央値インフレ率やダラス連銀の刈込平均インフレ率のような、業種を問わず大きな価格変化を除いた指標だった。こうしたコア指標は平滑な経路を辿り、2020年の経済が弱い時に徐々に低下し、その後経済が回復するにつれ上昇した。

以下は論文の図。

なお、このように変動を刈り込んでいくことの陥穽についてはこちらで紹介したスティーブン・ローチの警告も参照。