と題した記事でドイツ証券のレポートをFT Alphavilleが紹介している(原題は「Europe (still) not Japan, charted」)。

The difference between Europe today and Japan in the 1990s has become more pronounced than it was a few months ago…

A Japan-type dynamic could be defined as a situation in which private sector deleveraging is slow and is not accommodated by either aggressive fiscal nor monetary policy. As a result, the credit impulse (i.e. the pace of deleveraging) never reverses, and domestic demand remains under pressure. Ultimately, the economy converges to a situation in which inflation is negative and the output gap is widening while real interest rates are too high.

This is not happening in Europe. The GDP deflator is now above 1% while it remained persistently in negative territory in Japan. The unemployment rate is declining (from elevated levels) while in Japan it was just beginning its long ascent. The turnaround in Europe is occurring thanks to more complete deleveraging of the private sector, a more aggressive monetary policy, a weaker currency and a fiscal policy which has turned neutral after having tightened too quickly too early. In short, Europe is now in a position in which real rates are low, the currency is cheap, growth is above potential, the unemployment rate is declining and the deleveraging of the private and public sectors is largely completed. More ECB easing may be necessary, but this will be in response to external factors rather than a weak domestic dynamics.

(拙訳)

今日の欧州と1990年代の日本との違いは、数ヶ月前よりも明確になっている。・・・

日本型推移は、民間部門の負債圧縮が遅く、積極的な財政もしくは金融政策でサポートされていない状況として定義される。その結果、クレジット・インパルス*1(即ち、負債圧縮のペース)が逆転することはなく、国内需要は重荷を抱えたままとなる。最終的に経済は、インフレ率がマイナスで生産ギャップが拡大し、実質金利が高すぎる状況に陥ることになる。

これは欧州では起きていない。GDPデフレーターは現在1%を超えているが、日本では継続的にマイナスの領域にあった。失業率は(高い水準から)低下しつつあるが、日本では長く上がり続けた。欧州が好転したのは、民間部門のより徹底した負債圧縮、より積極的な金融政策、より弱い通貨、そしてあまりにも早期かつ急速に引き締めすぎた後に中立に転じた財政政策のお蔭である。要するに今の欧州は、実質金利が低く、通貨が安く、成長が潜在力を超えており、失業率が低下しつつあり、官民の負債圧縮が概ね完了した状態にある。ECBによるさらなる緩和は必要となるだろうが、それは、域内の動向の弱さではなく外部要因への対応ということになるだろう。

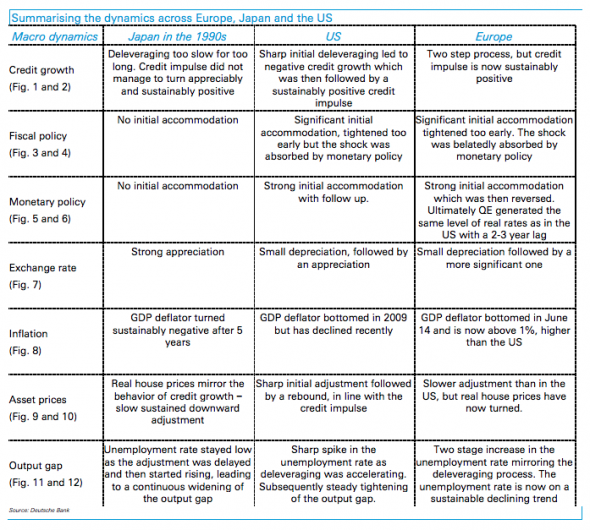

記事ではレポート中の以下の日米欧の対応表も合わせて引用し、欧州は1990年代の日本というよりは2-3年前の米国に近い、と書いている。

*1:このサイトの説明によると:

Michael Biggs, economist at Deutsche Bank, introduced this idea in Nov 2008 and, by analogy with the well known concept of fiscal impulse, defined “credit impulse” as the “the change in new credit issued as a % of GDP”. Since 2008, it has been shown, for many time periods and many countries, that private sector demand is very closely correlated with private sector credit impulse. This explains a number of conundrums missed by those who focus on the credit stock.