というNBER論文が上がっている(ungated(SSRN)版)。原題は「Tariff War Shock and the Convenience Yield of US Treasuries — A Hedging Perspective」で、著者はViral V. Acharya(NYU)、Toomas Laarits(同)。

以下はその要旨。

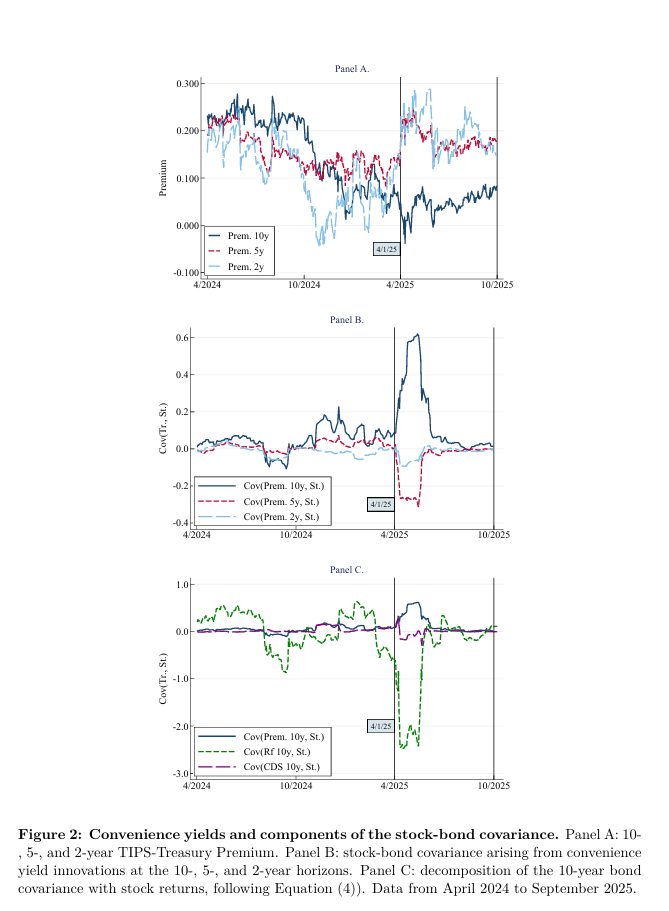

We explain how the “Tariff War” shock of April 2025 affected the safe-asset status of US Treasuries. Convenience yield erosion for long bonds is consistent with a reduction in the hedging property, reflected in a rising stock-bond covariance. Decomposing the Treasury yield into risk-free rate, credit spread, and convenience yield components reveals that covariance due to the convenience yield component increased for long bonds. The short end of the Treasury curve, however, continued to exhibit the safe-asset hedging property. These effects are consistent with a withdrawal of safe-asset investors from long-term Treasuries and a rotation towards shorter-term Treasuries and gold.

(拙訳)

我々は、2025年4月の「関税戦争」ショックがどのように米国債の安全資産の地位に影響したかを説明する。長期債のコンビニエンスイールドの減衰は、株債の共分散の上昇に反映されたヘッジ特性の減少と整合的である。国債利回りを無リスク金利、信用スプレッド、およびコンビニエンスイールドに要因分解すると、コンビニエンスイールド要因に起因する共分散が長期債について上昇したことが分かる。ただ、国債利回り曲線の短期側の端は安全資産のヘッジ特性を示し続けた。こうした効果は、安全資産の投資家が長期国債から手を引き、より短期の国債と金にシフトしたことと整合的である。

以下は10年債のコンビニエンスイールドの低下(2年債、5年債はむしろ上昇)、株との共分散上昇(2年債、5年債はむしろ低下)、共分散の要因分解を示した論文の図。