前回エントリで紹介したブランシャールのインフレ論にMITのIvan Werningが反応し、自分の研究を紹介する連ツイを立てている。

Olivier is making an important point that inflation comes from distributional conflict, but getting a lot of pushback. In my view misplaced.

This prompts me to share some research that explores this view of inflation with Guido Lorenzoni.

The analysis is done with a completely standard component of a macro New Keynesian (Calvo) model, and could be adapted to many other settings.

Inflation emerges from wage and price setters disagreeing on W/P aimed for and try to outdo each other, pushing up nominal prices/wages.

The main positive contribution is to show under what conditions W/P can go down in a "wage price spiral" (also to explain one version of what that may mean).

This happens when the excess demand is on the goods market side (inputs) and when prices are relatively more flexible than wages. We have a simple condition for this. I won't get into details here...

Here is an early draft. More results and normative analysis to come, stay tuned, will be updating this thread and the draft soon.

Here is a presentation slide deck...

Let me end mentioning one result that is not so obivous: stronger excess demand can cause real wages to fall more, as prices move up more quickly...

Oops forgot to tag Guido @guido_lorenzoni

Might also interest @MacRoweNick @t_holden @JohnHCochrane

Thanks!

(拙訳)

オリビエはインフレが分配上の軋轢に起因するという重要な指摘を行ったが、多くの反論を招いている。私に言わせればそれらの反論は筋違いである。

それで私は、インフレについてのそのような見解をグイド・ロレンツォーニと一緒に追究した研究をシェアしようという気になった。

分析は、マクロ経済学のニューケインジアン(カルボ)モデルの完全に標準的な構成要素によって行っており、数多くの別の状況に適応できる。

インフレは、賃金と価格の設定者が目標とするW/Pについて意見が一致せず、お互いを出し抜こうとして名目価格/賃金を押し上げることから生じる。

論文の主な貢献は、どのような条件下でW/Pが「賃金物価スパイラル」に陥るかを示したことにある(それが何を意味するかについての一つの解釈も説明している)。

これが起きるのは、財市場(投入)側で需要超過が生じ、価格が賃金に比べて伸縮的な場合である。これについては簡単な条件式があるが、ここでは詳細について深入りしない。

初期段階の原稿はこちら。結果と規範的分析を今後追加するので、乞うご期待。このスレッドと原稿を直にアップデートするつもり。

www.dropbox.com

プレゼン資料はこちら。

www.dropbox.com

最後にそれほど自明でない結果を一つ述べておこう。超過需要が大きいと、実質賃金の低下は大きくなる。物価の上昇の方が速いためだ…。

おっと、グイドにメンションするのを忘れてた。

あとNick Rowe、Tom Holden、ジョン・コクランも興味を持つかな。

多謝!

このツイートはリカルド・ライス(Ricardo Reis)のツイート(H/T 一上響氏)の中で引用されているものだが、そのライスのツイートは以下の通り。

*** Inflation and wages

A long time ago, Jordi Gali, Mark Gertler and Argia Sbordone noted: with sticky prices, inflation is expected to accelerate when marginal costs are temporarily low. Intuitively, costs will rise back, and as they do, firms will raise prices.

🧵1/12

This is sometimes called a New-Keynesian Phillips curve (not quite accurate as this is the optimal pricing condition from firms, no GE to link to real activity)

E_t ( 𝛽 𝜋_{t+1} - 𝜋_t) = - 𝜆 rmc_t

(all variables are deviation from steady states)

2/12

But how to measure marginal costs? Gali-Gertler-Sbordone noted that if labor is the variable input, then the labor share of income in the non-farm business sector could be a good proxy. And they found a pretty good econometric fit of this condition.

3/12

In 2022 the US labor share has fallen a lot. Wages rose less than prices. Inflation did not fall, but rose in 2022, which in the NK model would happen because of accommodative monetary policy. Now, you'd expect a lot of inflation for 2023. You can call it a wage-price spiral

4/12

The problem with this prediction is empirical. Below is the growth rate of the labor share over the last 20 years when inflation was at 2%. While 2022 inflation is an 8-standard deviation event, the 2022 labor share deviation does not really stand out.

5/12

At the same time, the labor share had been falling since 2000 and then recovered sharply in 2016-20. Is it right now below or above where it might be on average over the next decade? Is the fall in 2022 due to inflation or rather tech/globalization?

6/12

https://annualreviews.org/doi/pdf/10.1146/annurev-economics-080921-103046

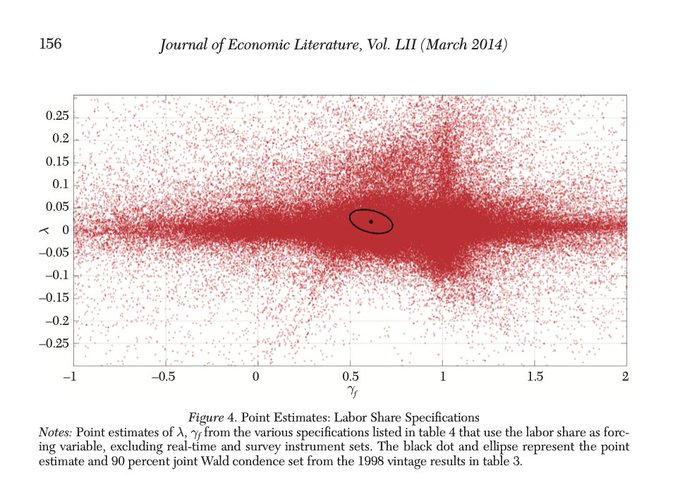

The Gali-Gertler-Sbordone regression has not stood well. Conceptually, the labor share is a poor proxy for marginal costs. Empirically, the data just cannot identify it influence on inflation accurately. From a 2014 survey estimates of 𝜆:

7/12

https://aeaweb.org/articles?id=10.1257/jel.52.1.124

This thread comes from reading a great new paper by @IvanWerning and @guido_lorenzoni. They unpack the labor share more deeply as a conflict between wages (or mrs) and the marginal product of labor, work through how it adjusts with inflation, and more

8/12

FWIW, I'm on their side in using the word conflict: after all, we are talking about the workers’ share of national income.

There's a fundamental indeterminacy of inflation. The central bank's policy coordinates the expectations of conflicting agents.

9/12Stumbled upon this article by @R2Rsquared and @lcastillomart on how central banks control inflation. Very relevant as a thought organizer for the many inflation discussions taking place today.

— Nirai Tomass (@gmmengineer) 2022年12月26日

Still a bit perplexed, but not as much. So I recommend.https://t.co/FZ1KBgEAMH pic.twitter.com/r9ITdp0y9i

A different take on the conflict caused by (rather than causing) inflation: in the last 6 months in the UK, there were multiple strikes per week, as every union tried to get its wage reset.

Menu costs for wages are real strikes! @ojblanchard1

Beyond debates on what drives, causes and is caused by inflation:

Will the labor share and worker-firm conflicts matter for inflation in 2023-24?

Theory tells me so, but the empirical failure of linking labor share to inflation that I described gives me a lot of doubts.

11/12

I have mentioned this a lot in public lectures and panels in the last 6 months:

Wages are the key variable that I am looking at right now to figure out if inflation is going to fall in 2023.

(Yes, even more than inflation expectations! 😃)

12/12 end of 🧵

(拙訳)インフレと賃金

その昔、ジョルディ・ガリ、マーク・ガートラーとアルジア・スボードンは次のように述べた:物価が粘着的な場合、インフレは限界費用が一時的に低いと加速すると予想される。直観的に言えば、費用は再上昇すると予想され、実際にそうなると企業は価格を引き上げる。

それは時にニューケインジアンフィリップス曲線と呼ばれる(これは企業側の最適価格設定条件であり、実体経済活動に結び付く一般均衡は無いので、必ずしも正しい呼び方ではない)。

E_t ( 𝛽 𝜋_{t+1} - 𝜋_t) = - 𝜆 rmc_t

(すべての変数は定常状態からの乖離)

ideas.repec.org

しかし限界費用をどのように測定するのか? ガリ=ガートラー=スボードンは、労働が可変投入量ならば、非農業部門における所得の労働分配率が良い近似になる、と述べた。そして彼らは、この条件が計量経済学的に非常に良くあてはまることを見い出した。

ideas.repec.org

2022年に、米国の労働分配率は大きく下落した。賃金の上昇は物価よりも小さかった。インフレは2022年に下落せずに上昇したが、これはニューケインジアンモデルでは緩和的な金融政策により生じる。これから2023年には大きなインフレが生じると予想されるだろう。賃金物価スパイラルと呼んでも良いかもしれない。

その予測の問題点は実証的なものだ。以下は、インフレ率が2%だった過去20年の労働分配率の伸び率だが、2022年のインフレが8標準偏差の出来事だったのに対し、2022年の労働分配率の乖離はそれほど目立つものではない。

また、労働分配率は2000年以降低下した後、2016-20年に急速に回復した。今は、今後10年間の平均に比べて低いのか高いのか? 2022年の低下はインフレのせいか、それとも技術ないしグローバリゼーションのせいか?

https://annualreviews.org/doi/pdf/10.1146/annurev-economics-080921-103046

ガリ=ガートラー=スボードン回帰は状況の変化にあまり耐えられなかった。概念的に労働分配率は限界費用の代理変数としてあまり良くない。そのインフレへの影響が、実証的にデータから正しく識別できないのである。2014年の研究におけるλの推定は以下の通り。

https://aeaweb.org/articles?id=10.1257/jel.52.1.124

このスレッドはイヴァン・ワーニングとグイド・ロレンツォーニの素晴らしい新たな論文を読んだことで生まれた。彼らは労働分配率を、賃金(ないし限界代替率)と労働の限界生産物との軋轢としてより深く分析し、それがインフレにどのように適合するか、といったことなどを研究した。Olivier is making an important point that inflation comes from distributional conflict, but getting a lot of pushback. In my view misplaced.

— Ivan Werning (@IvanWerning) 2022年12月31日

This prompts me to share some research that explores this view of inflation with Guido Lorenzoni. https://t.co/6tEYhzja11

ちなみに私も軋轢という言葉を彼らと同じ意味で使っている。結局のところ、我々は国民所得の労働者の分け前について話しているのである。

インフレには根本的な不確定性があり、中銀は軋轢のある主体の予想を一致させる。(Nirai Tomassのツイート)

中銀のインフレのコントロール法に関するリカルド・ライスとLaura Castillo-Martinezによる以下の論文を見つけた。今日交わされている数多くのインフレに関する議論について考えをまとめる上で非常に重要。

まだ少し混乱しているが、以前ほどではなくなった。ということでお勧め。

https://personal.lse.ac.uk/reisr/papers/99-perplexed.pdf

インフレ(を引き起こすのではなく)で引き起こされる軋轢についての違う見方。英国では過去6か月の間に週当たり複数のストライキがあった。全ての組合が賃金の再設定を求めた。

賃金のメニューコストは実際のストライキなのだよ、ブランシャール!1/8. A point which is often lost in discussions of inflation and central bank policy. Inflation is fundamentally the outcome of the distributional conflict, between firms, workers, and taxpayers. It stops only when the various players are forced to accept the outcome.

— Olivier Blanchard (@ojblanchard1) 2022年12月30日

何がインフレを駆動し引き起こすか、インフレによって何が引き起こされるか、の議論はともかく、2023-24年のインフレにとって、労働分配率と、労働者と企業の軋轢は重要だろうか?

理論はそうだと言っているが、上で説明したように労働分配率とインフレとを実証的に結び付けるのは上手くいっていないので、私はかなり疑念を抱いている。

過去6か月に公開講義やパネル討論で大いに述べたことだが、今現在、インフレが2023年に低下するかどうかを見通す上で、賃金こそが私の注目する指標である(そう、インフレ予想よりもね!)。

今回と前回のエントリで紹介したインフレ論を日本に当てはめるならば、日本では賃金を上げようという動きが昨今の物価上昇を経てもかなり鈍いので、主体間の軋轢は未だ起きず、軋轢の調停者としての中銀の出る幕が今のところ無い*1、ということになろうか。

*1:むしろ、一部の反リフレ派の煽りもあり、物価上昇に寄与したという恨みを中銀が集めて賃金上昇を求める勢いをややガス抜きする結果になっているかもしれない。