スタンリー・フィッシャーが、ウォーリック経済サミット*1での「I'd Rather Have Bob Solow Than an Econometric Model, But ...」と題した11日の講演で、金融政策の決定過程について解説している(H/T Economist's View)。

Eureka moments are rare in all fields, not least in economics. One such moment came to me when I was an undergraduate at the London School of Economics in the 1960s. I was talking to a friend who was telling me about econometric models. He explained that it would soon be possible to build a mathematical model that would accurately predict the future course of the economy. It was but a step from there to realize that the problems of policymaking would soon be over. All it would take was a bit of algebra to solve for the policies that would produce the desired values of the target variables.

It was a wonderful prospect, and it remains a wonderful idea. But it has not yet happened. I want to talk about why not and about some of the consequences for policymaking.

(拙訳)

どの分野でも、分かった!という瞬間が訪れるのは稀だが、経済学でもそうである。そうした瞬間の一つが私に訪れたのは、1960年代にロンドン経済学院の学部生だった時のことだった。私は友人と会話していて、その友人は計量経済モデルについて私に教えてくれていた。彼は、経済の先行きを正確に予測する数学モデルを構築することが間もなく可能になるだろう、と説明した。その話をもう一歩推し進めれば、政策決定の問題も直に片が付く、ということに私は気が付いた。目標変数を望ましい値に持っていく政策を求めるのは、少々の数学があれば良い、というわけだ。

それは素晴らしい展望であり、今も素晴らしい考えであることには変わりない。しかしそれは未だに実現していない。今日は、それが実現していない理由と、政策決定におけるその影響についてお話ししたい。

この後フィッシャーは、FOMCにおける政策決定プロセスと、FOMCのためにスタッフによって用意される2部構成の資料(ティールブック)、およびFRB/USモデルについて説明した上で、実例を挙げている。

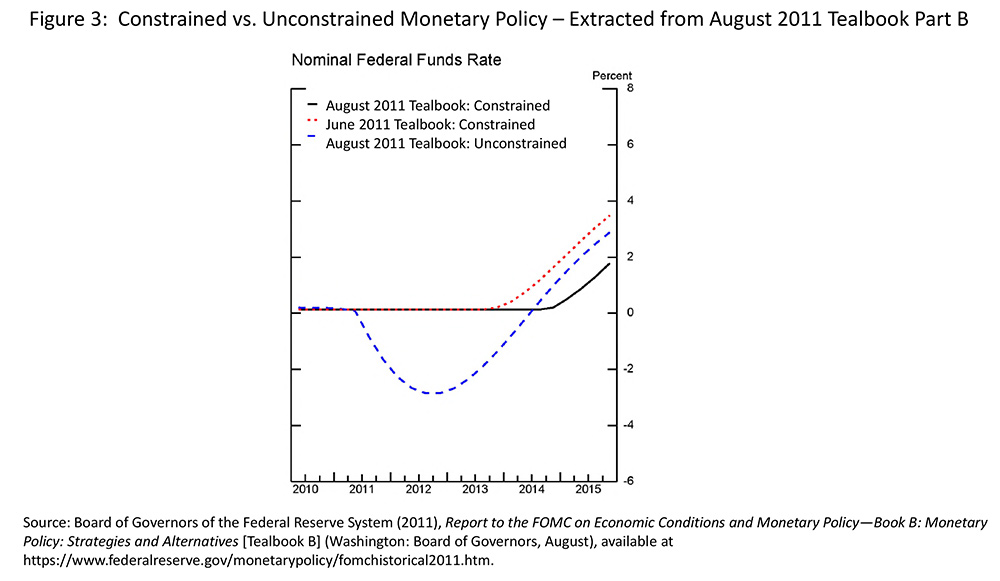

As an example of such a process, I want to discuss the important decision taken at the August 2011 meeting. At the time policymakers gathered in Washington for the meeting, the FOMC's target for the federal funds rate had been set to nearly zero for more than 2-1/2 years. And although the economy had improved from the depths of the Great Recession, the unemployment rate was still above 9 percent.

Over the summer, the economic outlook darkened considerably. In response, in August, the staff's Tealbook forecast projected that the federal funds rate would remain near zero three quarters longer than what the staff had expected in June. Figure 3, taken from the August 2011 Tealbook, illustrates how the change in the economic outlook affected FRB/US simulations of optimal monetary policy. As you know, an optimal policy is a path for the policy instrument that minimizes the shortfalls in economic outcomes relative to policymakers' goals; in this case, the optimal policy path is computed using the FRB/US model and takes the staff's baseline outlook as given. In principle, optimal policy simulations deliver better outcomes than simple policy rules, but those outcomes are conditional on some strong assumptions.

...the prescriptions of optimal policy were saying not only that the Committee's interest rate should remain at zero for some time to come, but also that that period of time should be considerably longer than previously thought.

(拙訳)

そうしたプロセスの例として、2011年8月になされた重要な決定について説明したい。会合のため政策担当者がワシントンに集まった時、FOMCのFF金利目標は2年半以上ゼロ近傍に据え置かれていた。経済は大不況の底からは改善していたものの、失業率は依然として9%を超えていた。

夏に掛けて経済の見通しは一段と悪化した。そのため、8月のティールブックでのスタッフ予測では、6月時点の予測に比べて3四半期長くFF金利がゼロ近傍に留まる、との見通しを示していた。図3は2011年8月のティールブックから採られたものだが、経済見通しの変化がどのようにFRB/USの最適金融政策シミュレーションに影響したかを示している。ご承知の通り、最適政策とは、政策担当者の目標と比べた経済的帰結の落ち込みを最小化するような政策手段の経路である。この場合、最適政策経路はFRB/USモデルを使って計算され、スタッフのベースライン予測を所与のものとしている。原則として、最適政策シミュレーションは単純な政策ルールよりは良い結果をもたらすが、そうした結果は幾つかの強い仮定を条件としている。

・・・最適政策から導かれたのは、委員会の金利は当面の間ゼロに留まるべき、ということだけではなく、その期間は以前考えられていたよりも相当長くなる、ということであった。

結局、このFOMCでは、フォワードガイダンスに関する表現を強める(「for an extended period」→「at least through mid-2013」)ことが決定された。

And what do I take from this episode? The interest rate decision taken in August 2011 was unusual in that a decision was made about the likely path of future interest rates. Most often, the FOMC is deciding what interest rate to set at its current meeting. Either way, in reaching its decision, the Committee will examine the prescriptions of different monetary rules and the implications of different model simulations. But it should never decide what to do until it has carefully discussed the economic logic that underlies its decision. A monetary rule, or a model simulation, or both, will likely be part of the economic case supporting a monetary policy decision, but they are rarely the full justification for the decision. Sometimes a monetary policy committee will make a decision that is not consistent with the prescriptions of standard monetary rules--and that may well be the right decision. Further, in modern times, the policy statement of the monetary policy committee will seek to explain why the committee is making the decision it is announcing. The quality of those explanations is a critical part of the policy process, for good decisions and good explanations of those decisions help build the credibility of the central bank--and a credible central bank is a more effective central bank.

(拙訳)

このエピソードの教訓は何だろうか? 2011年8月に採られた金利に関する決定は、将来の金利の想定経路についての決定という点で異例であった。FOMCはその回の会合での金利を決定するのが通例である。いずれにせよ、FOMCは決定に到達するまでに、異なる金融ルールの下での政策、および、異なるモデルシミュレーションの含意を吟味する。しかし、何をするかを決定するのは、決定の基盤となる経済的論理を注意深く議論してから初めて行うべきである。金融ルール、もしくはモデルシミュレーション、もしくはその両方は、金融政策決定を支持する経済的主張の一部とはなるであろうが、決定を完全に正当化するものとなることは稀である。金融政策委員会が標準的な金融ルールから導かれる政策と矛盾する決定を下し、かつ、その決定が大いに正しい、ということもある。また、現代においては、金融政策委員会の政策ステートメントは、公表する決定を委員会が下した理由を説明しようとする。そうした説明の質は、政策プロセスの極めて重要な部分である。というのは、優れた決定と、そうした決定の優れた説明は、中央銀行の信認を構築するのに役立つからである。そして、信認の高い中央銀行は、より効果的な中央銀行なのである。

フィッシャーは講演を以下のように結んでいる。

As the August 2011 meeting illustrates, the eureka moment I thought I had 50-plus years ago was a chimera. Why is that? First, the economy is very complex, and models that attempt to approximate that complexity can sometimes let us down. A particular difficulty is that expectations of the future play a critical role in determining how the economy reacts to a policy change. Moreover, the economy changes over time--this means that policymakers need to be able to adapt their models promptly and accurately in real time. And, finally, no one model or policy rule can capture the varied experiences and views brought to policymaking by a committee. All of these factors and more recommend against accepting the prescriptions of any one model or policy rule at face value.

And now to the bottom line: The title of my speech is an incomplete quotation of something Paul Samuelson once said. What Samuelson said was this, "I'd rather have Bob Solow than an econometric model, but I'd rather have Bob Solow with an econometric model than without one." And Samuelson, who was a shameless eclectic, would almost certainly have said essentially the same thing about policy rules.

(拙訳)

2011年8月の会合が示すように、50云年前に私が分かったと思った瞬間は、幻想であった。それはなぜか? 第一に、経済は非常に複雑であり、その複雑さを近似しようとするモデルが期待に応えられないこともしばしばある。特に難しいのは、政策変更に経済がどのように反応するかを決める上で、将来への期待が極めて重要な役割を演じる点である。また、経済は時間とともに変化する。そのことが意味するのは、政策担当者も自分のモデルをリアルタイムで即座かつ正確に適応させることができねばならない、ということである。そして最後に、一つのモデル、もしくは一つの政策ルールだけで、委員会の政策決定に持ち込まれる様々な経験や見解を捉えることはできない。以上の要因すべてが他の要因と相俟って示しているのは、一つのモデル、もしくは一つの政策ルールから導かれる政策を額面通り受け入れるべきではない、ということである。

ここで話をまとめよう。私の講演のタイトルは、ポール・サミュエルソンがかつて述べた言葉の不完全な引用である。サミュエルソンの言葉は、「計量経済モデルよりはボブ・ソローが欲しいが、計量経済モデル抜きのボブ・ソローよりは計量経済モデル付きのボブ・ソローが欲しい」というものだった。清々しいほど折衷主義的だったサミュエルソンならば、政策ルールについても基本的に同じことを述べたに違いない。

*1:cf. ウォーリック大学 - Wikipedia。